Premium Priced Strategic Acquisitions

Despite persistent financial and geopolitical risk, M&A activity for 2014 in the photonics industry and vertical markets served surpasses that of the previous five years. Having been through a long period of organic growth, strategic buyers turn to M&A to keep growing – creating more competition for financial buyers and improving valuations.

So far this year, a handful of lower middle market companies with strong IP portfolios realizing premium valuations from strategic buyers are driving-up average Enterprise Value/Revenues multiples.

Leading the pack are: Selah Genomics, a nanotechnology company commercializing bio-sensing contrast agents that replace fluorescent dyes and quantum dots for biomedical and anti-counterfeiting applications (56x); Airinov, a provider of agronomic drone solutions based on optical sensor technology (38x); Plextronics, a developer of printed lighting, display, solar, and other organic electronics (20x); Fusion IP who commercializes third-party IP via investments in spin-out companies (128x), and Q-Chip, a biopharmaceutical drug delivery company (160x).

The Transactions

M&A transactions are researched with closing or announce dates from January 1 to December 31, 2014. Transactions volumes, values, geographies, and market segments are analyzed. Values are in $US at historical rates of exchange. Follow this link to transaction detail. <2014 Photonics M&A Transactions>

Activity

The Materials & Coatings, LED Packages & Luminaires, Display, and Solar market segments saw the most activity in volume of transactions.

M&A Transaction Volume

Photonics & Vertical Markets Served

2014

In 2014, the total and average Enterprise Value of the 430 transactions reporting financial data were $190 billion and $462 million respectively.

M&A Transaction Value

Photonics & Vertical Markets Served

2014

Photonics Core Technology Companies

Unprecedented in the previous five years, the Photonics sector saw at least as much, if not more, activity in the volume of transactions than the market sectors it enables.

With the exception of camera systems suppliers, Andor, Opus and SmallHD, target companies in Cameras, Detectors, and Sensors segment are manufacturers of component level sensors – predominantly CMOS.

In the Lasers segment, quantum cascade lasers (QCL) debuted. ThorLabs acquires Corning’s QCL product line. Emerson acquires Cascade Technologies, a QCL-based gas analyzer supplier.

Recent advances in commercially available materials and their related photonics technologies are driving innovation in lighting, life sciences, IT, energy, and construction. 2014 saw suppliers of fundamental materials such as quantum dots, phosphors, carbon, fullerene, polymer additives, rare earths, semiconductors, and nanoparticles being acquired. The scarcity of rare earths is addressed by target companies in 2014 – DELA, a recycling technology company that recovers rare earth metals; Coltide, manufacturer of X-ray fluorescence drift monitors for mining companies; and Grirem of China, developer and produced of rare earth and related materials.

The Optics segment also was more transactions in 2014. Leading the pack in volume are target companies supplying free-space optical lens systems and micro-optic components and subassemblies for cameras, display backlights, and medical devices. The most strategic acquisitions were for companies supplying active switching components and illumination optics amenable to applications in Display, Lighting and Information Technology. Active switch and filter companies include Boulder Non-Linear, 3S Photonics, Lake Shore Cryotronics, and Proximion. Illumination optics and films companies include NingBo DXC New Material Technology, Digital Optics, and LMS.

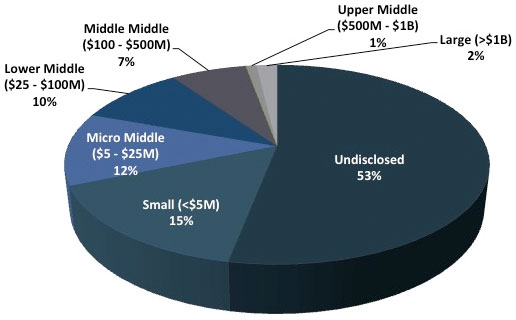

Small and Middle Market

47% of researched transactions disclosed the transaction value. Of those disclosed and consistent with previous three years, 79% are small market (<$5M), micro middle market ($5 to $25M), and small/middle market ($25 to $100M) transactions.

Since 2010, the lower and middle of the M&A middle markets remain robust. These researched transactions are consistent with that market as a whole. However, uniquely, in the Photonics sector and the vertical market segments enabled by photonics, strategic buyers are acquiring orders of magnitude smaller businesses providing products that are highly differentiated with strong intellectual property positions.

M&A Transaction Size

Photonics & Vertical Markets Served

2014

Strategic vs. Financial on Buy and Sell Side

Like 2012 and 2013, the vast majority of transactions by volume and value are strategic. However, financial buyers and sellers are consistently more active since 2012 – financial buyers up to 17% from 3% of transactions and financial sellers up to 17% from 12%. Considering strategic buyers are more active in 2014, this is a seller’s market with higher strategic premiums in valuations for both strategic and financial buyers.

Valuations

For researched market segments enabled by photonics technologies, the average and median of reported Enterprise Value to EBIT, EBITDA and Revenue multiples in 2014 trend higher since 2012 and 2013. Implied Enterprise Value includes implied equity value, earn-out and contingent payments, rights, warrants, options, and net assumed liabilities adjusted for size.

The Materials & Coatings (Photonics), Medical Imaging (Biophotonics), and Surveillance & Navigation (Defense, Security & Sensing) segments realize the highest average multiples of Enterprise Value to Revenue due to strategic acquisitions of lower middle market companies with strong IP portfolios.

The Semiconductor Equipment (Advanced Manufacturing), Display (Information Technology), and Solar (Energy) segments realize the highest average multiples of Enterprise Value to EBITDA. Highest multiples were realized across multiple market segments by Tera Semicon, a manufacturer of Chemical Vapor Deposition (CVD) semiconductor equipment used to manufacture Liquid Crystal (LCD) and Active Matrix Organic LED (AMOLED) displays, LED’s and solar cells (47x EBITDA); SMA Solar Technology, a provider of solar inverters (44x EBITDA); and Given Imaging, a supplier of gastrointestinal diagnostics products based on a proprietary wireless imaging system and disposable video capsules (34x EBITDA).

Few transactions report financials, because buyers are not required if a transaction does not have material near term impact on their financial statements. M&A transaction data is highly relevant, however, to understand market dynamics and buyer behavior.

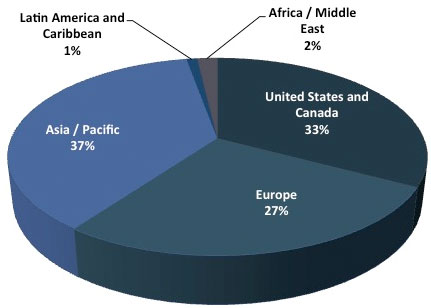

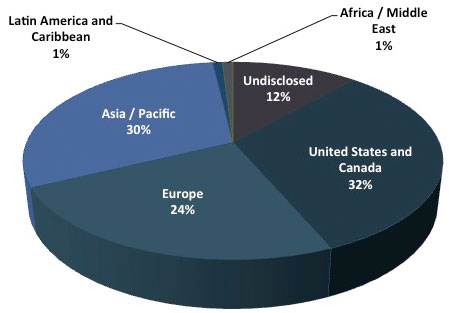

Geography

Historically, the United States and Canada, as a geographical region, experience the most buy and sell side activity.

M&A Transactions by Geography – Target

Photonics & Vertical Markets Served

2014

M&A Transactions by Geography – Buyer

Photonics & Vertical Markets Served

2014

More than 25% of transactions represent buyers acquiring targets outside their geographical region.

Most Active Buyers

Financial buyers in Korea were by far the most active – acquiring small and middle market optics, laser, and materials companies. Another 5 strategic buyers, including 3D Systems, Tianma, Corning, Stratasys, and EKF Diagnostics, acquired at least 4 entities each. Unprecedented in 2014 is the relatively large number of acquisitions per strategic buyer.

Following the eight-figure consolidations of the medical diagnostics businesses of Life Technologies by Thermo Fisher and Sigma Aldrich by Merck, the largest transactions in 2014 were: The Carlyle Group’s acquisition of Johnson & Johnson’s Ortho-Clinical Diagnostics; Zebra’s acquisition of Motorola’s business including laser/image ID capture product lines; Corning’s acquisition from Samsung of Korea based supplier of inorganic materials and TFT-LCD glass substrates for displays and solar devices, and thermochromic coated glass/solar light control glass; Facebook’s acquisition of Oculus VR, a manufacturer of wearable immersive virtual reality technology future proofing a social media platform.

The Transactions

Follow this link to transaction detail. <2014 Photonics M&A Transactions>