Beyond Compliance Toward Relevance & Better Financing Decisions

Understanding today’s expected rate of return for private capital from venture capital to private equity to asset based lenders, premiums paid for businesses by strategic buyers, and industry dynamics help business valuation professionals advise business owners in making better investing and financing decisions.

The Private Cost of Capital Model (PCOC) is based on the expected rate of return that private capital markets require in order to attract funds to a particular investment. This model enables appraisers and others to directly derive private business values from private return expectations, allowing a more relevant comparison – as opposed to solely documenting business value for compliancy.

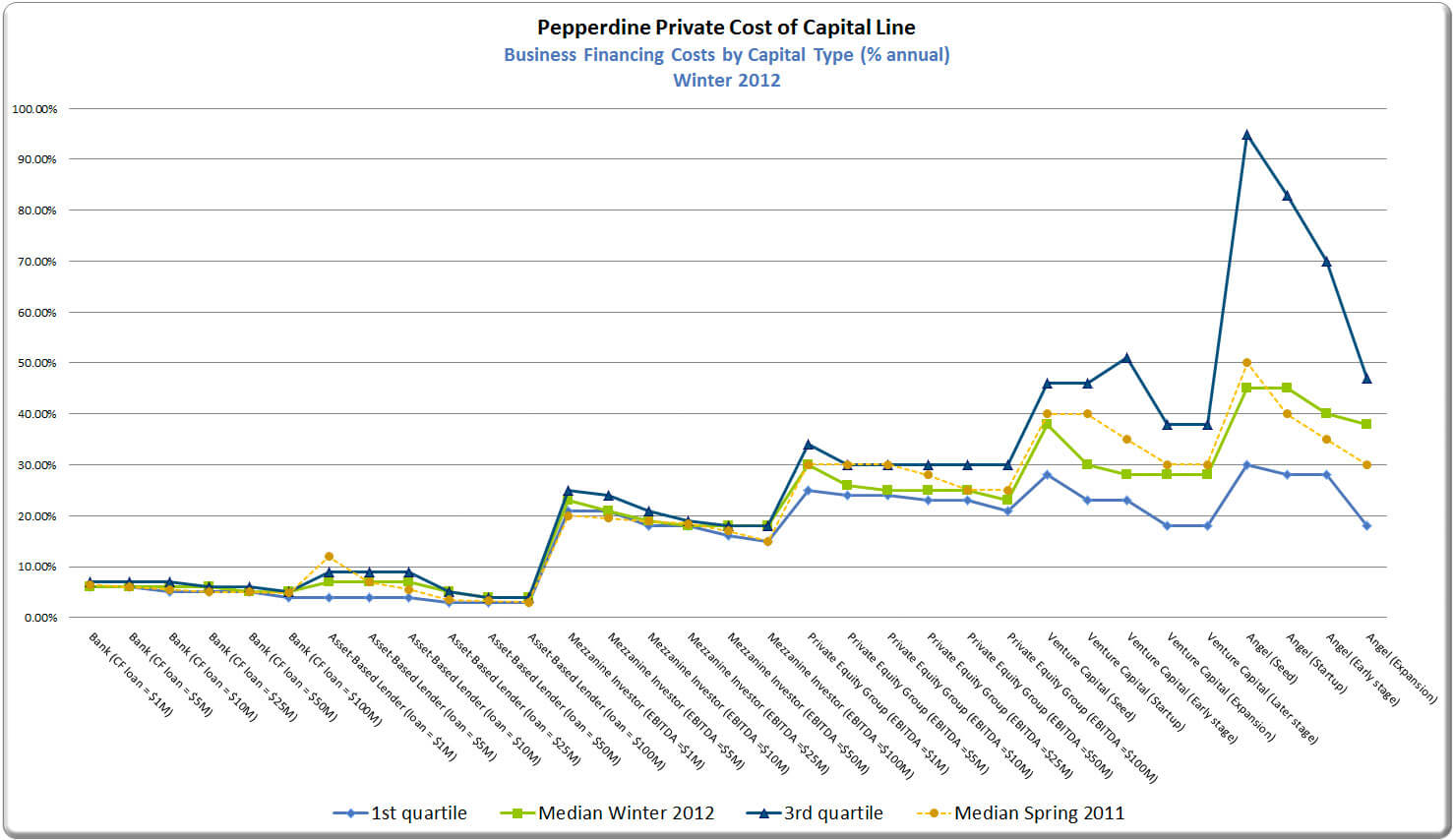

Pepperdine PCOC Survey

The Pepperdine private cost of capital survey is a web based survey of tens of thousands of capital providers including banks, asset based lenders, mezzanine investors, private equity groups, venture capitalists, factoring companies, business owners, investment banks, and business valuation professionals.

The survey below, released in Winter 2012, investigated for each private capital market segment, the important benchmarks that must be met in order to qualify for capital – amount of capital typically accessible, required returns for extending capital in the current economic environment, and outlooks on demand for various capital types, interest rates, and the economy in general.

166 private equity firms responded to the survey. Approximately 43% reported typical investment size to be in the $10 million to $25 million range. According to respondents, the most important factors to consider when investing and determining the company specific risk premium are future prospects of the company and management team. Private Equity firms reported the following deal multiples of EBITDA paid in manufacturing industries – generally up from prior 6 months. The survey reported the following deal multiples of EBITDA by industry paid by financials buyers.

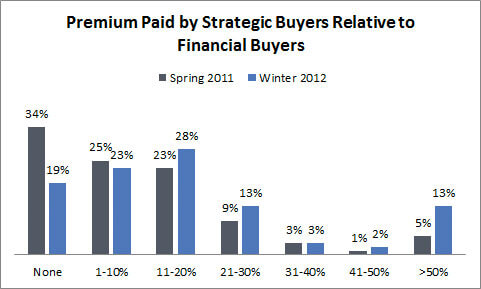

Investment bankers were asked if purchasing premiums were present when strategic buyers were involved. Approximately 81% of respondents, as opposed to 66% in the previous six month period, witnessed premiums paid by strategic buyers.

50% or more of investment bankers surveyed believed that deal multiples, exit business opportunities, and strategic buyers making deals increased slightly over the previous six month period and would continue to increase slightly in the next 12 months.

Public and Private Capital Markets are Not Substitutes

Today, public return data is used by appraisers to derive costs of capital for private company valuation. Corporate Finance Theory, grounded in assumptions around a single efficient public market, is also used by appraisers to value private companies – private companies that have no access to public markets and never plan to IPO.

Public companies use a C-Corporation with a goal to maximize profit. Their owners have limited liability, are well diversified, and employ a professional management team. On the contrary, private companies also use an S-Corporation, LLC or other entity. Owners have unlimited liability, are undiversified with typically one primary asset, and are often managing the business.

These fundamental dissimilarities make questionable the application of Corporate Finance Theory to valuing private businesses. They call for the development of new theories and compliance guidelines to predict risk and return, rational market behavior, equilibria, and utility for both small company and private capital markets.

The PCOC model derived from Private Capital Markets Theory applies to private companies with sales from approximately $5 to $500 million.

Private Cost of Capital Model

The Private Cost of Capital model is based on the principal of substitution and mirrors how private capital providers make investment decisions. The relevant market of investors is the market that determines the cost of capital. Discount rates emanate from the return expectations of the relevant capital providers.

Referencing the PCOC model below, the first step in determining the appropriate CAP is to review the credit boxes described in the most current Pepperdine survey. Next, select the appropriate median CAP from the survey results. Then, adjust the survey CAP by SCAPito reflect the company specific risk based on a comparison between the subject company and the survey. Use the upper and lower quartile returns as a guide to this adjustment.Determine the market value of each CAP and derive the percentage of the capital structure for each CAP. Finally, add the individual percentages to derive PCOC.

Compliance vs. Relevancy

Contrasting the PCOC model to Capital Asset Pricing Model and Build Up Method, questions around both fundamental theory and compliance arise. How will minority interest discounts be calculated? Is there a need for control premiums and discounts for lack of marketability? How will minority interests be calculated? Are there robust sources of private capital? Do they price risk? Is it possible to learn return expectations of individual private capital providers?

However, considering private capital market risk in business valuation can move business valuation more toward market relevancy. According to the Pepperdine survey, 80% of business owners are not generating a return on investment greater than their cost of capital. As opposed to solely documenting business value for compliancy, the PCOC model promises to help business valuation professionals advise business owners in making better investing and financing decisions

Sources: Slee, Rob and Paglia, John. “Private Cost of Capital Model.” The Value Examiner. March / April 2010.; Pepperdine Private Capital Markets Project – Survey Report VI – Winter 2012