Premium Priced Strategic Acquisitions & Consolidation

Given well-capitalized strategic buyers with large cash reserves, a better financing environment for private equity, and an improved macro-environment, M&A activity in 2014 is predicted more robust than in the past two years. In the photonics industry and vertical market segments employing its technologies as core differentiators, trends of consolidation and premium priced, strategic acquisitions persist into 2014.

So far this year, a handful of lower middle market companies with strong IP portfolios realizing premium valuations from strategic buyers are driving-up average Enterprise Value/Revenues multiples.

Leading the pack are: Selah Genomics, a nanotechnology company commercializing bio-sensing contrast agents that replace fluorescent dyes and quantum dots for biomedical and anti-counterfeiting applications (56x Revenue); Airinov, a provider of agronomic drone solutions based on optical sensor technology (38x Revenue); Plextronics, a developer of printed lighting, display, solar, and other organic electronics (20x Revenue); and Fusion IP who commercializes third-party IP via investments in spin-out companies (128x Revenue).

Multibillion-dollar deals are inked by Thermo Fisher Scientific, The Carlyle Group, Corning, and Facebook – strategic buyers consolidating medical diagnostics businesses, extending into new Gorilla Glass markets, and future proofing a social media platform.

The Transactions

M&A transactions are researched with closing, effective, or announce dates from January 1 to April 10, 2014. Transactions volumes, values, geographies, and market segments are analyzed. Values are in $US at historical rates of exchange. Follow this link to transaction detail. <2014 Jan to April Photonics M&A Transactions>

Activity

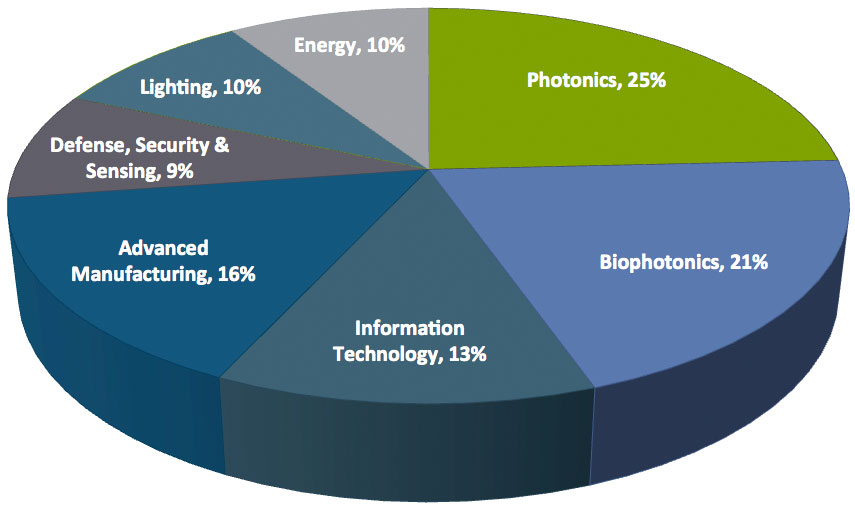

The Materials & Coatings, Medical Diagnostics, Display, and LED Luminaires segments saw the most activity in volume of transactions.

M&A Transaction Volume

Photonics & Vertical Markets Served

January – April 2014

In 2014, the total and average Enterprise Value of the 100 transactions reporting financial data are $43 billion and $414 million respectively. The total reported transaction value by sector is heavily weighted by a single large transaction in Biophotonics. Removing the $16billion Thermo Fisher acquisition from the analysis, the total volume and average value of transactions is in line with 2012 and the same period 2013 wtih Materials & Coatings, Medical Diagnostics, and Display segments realizing the most transaction value. Lighting and Energy segments combined see less than 5% of the total value of transactions.

M&A Transaction Value

Photonics & Vertical Markets Served

January – April 2014

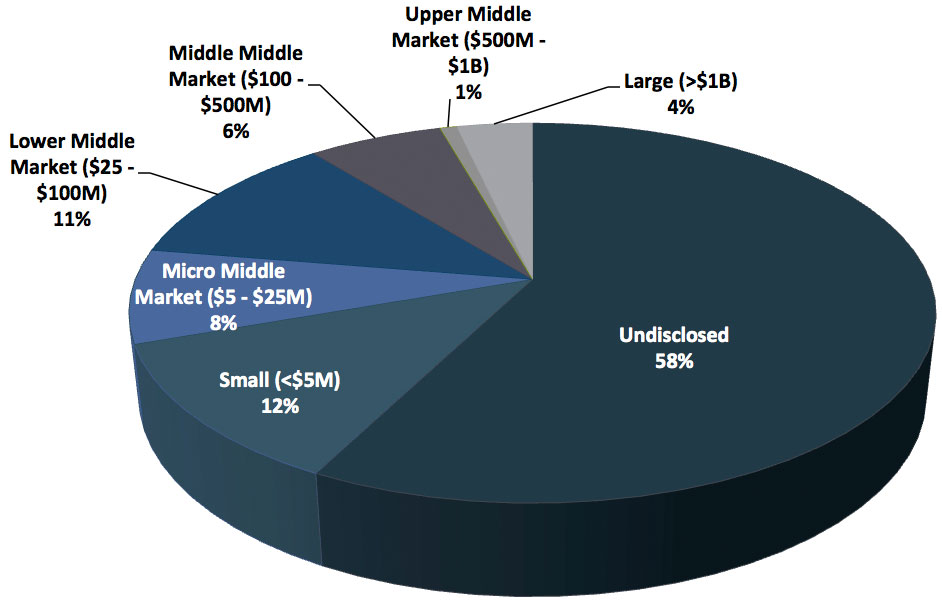

Small and Middle Market

42% of researched transactions disclose the transaction value. Of those disclosed, 75% are small market (<$5M), micro middle market ($5 to $25M), and small/middle market ($25 to $100M) transactions.

Since 2010, the lower and middle of the M&A middle markets remain robust. These researched transactions are consistent with that market as a whole. However, uniquely, in the Photonics sector and the vertical market segments enabled by photonics, strategic buyers are acquiring orders of magnitude smaller businesses providing products that are highly differentiated with strong intellectual property positions.

M&A Transaction Size

Photonics & Vertical Markets Served

January – April 2014

Strategic vs. Financial on Buy and Sell Side

Like 2012 and 2013, the vast majority of transactions by volume and value are strategic. However, financial investors are continuously more active since 2012 – financial buyers up to 17% from 3% of transactions and financial sellers up to 17% from 12% involving financial investment sellers. If strategic buyers are more active in 2014 as forecast, this is a seller’s market with higher strategic premiums in valuations for 2014.

Valuations

For researched market segments enabled by photonics technologies, the average and median of reported Enterprise Value to EBIT, EBITDA and Revenue multiples in 2014 trend higher since 2012 and 2013. Implied Enterprise Value includes implied equity value, earn-out and contingent payments, rights, warrants, options, and net assumed liabilities adjusted for size.

The Materials & Coatings (Photonics), Medical Imaging (Biophotonics), and Surveilliance & Navigation (Defense, Security & Sensing) sectors realize the highest average multiples of Enterprise Value to Revenue due to strategic acquisitions of lower middle market companies with strong IP portfolios.

The Semiconductor Equipment (Advanced Manufacturing), Display (Information Technology), and Solar (Energy) sectors realize the highest average multiples of Enterprise Value to EBITDA. Highest multiples were realized across multiple market segments by Tera Semicon, a manufacturer of Chemical Vapor Deposition (CVD) semiconductor equipment used to manufacture Liquid Crystal (LCD) and Active Matrix Organic LED (AMOLED) displays, LED’s and solar cells (47x EBITDA); SMA Solar Technology, a provider of solar inverters (44x EBITDA); and Given Imaging, a supplier of gastrointestinal diagnostics products based on a proprietary wireless imaging system and disposable video capsules (34x EBITDA).

Few transactions report financials, because buyers are not required if a transaction does not have material near term impact on their financial statements. For this reason, comprehensive valuation opinions rarely consider M&A transactions in their analysis. M&A transaction data is relevant, however, to understand market and buyer dynamics.

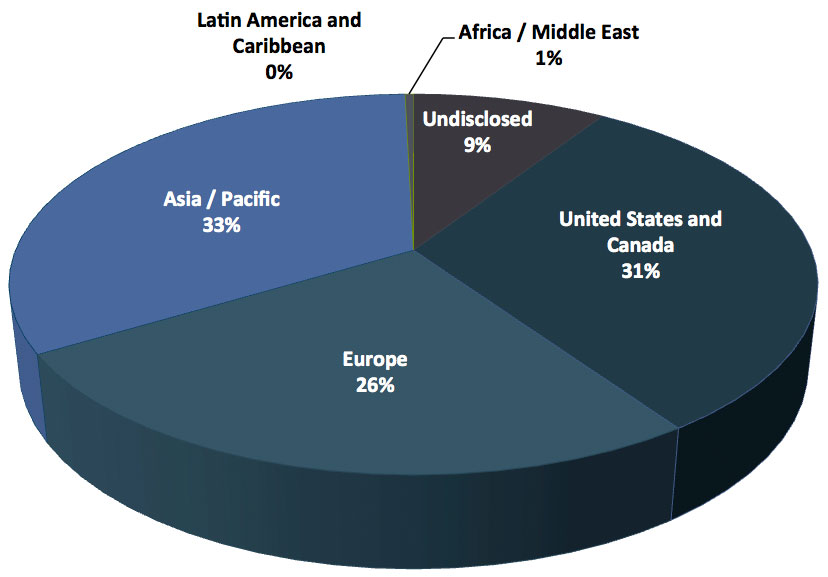

Geography

Historically, the United States and Canada, as a geographical region, experience the most buy and sell side activity. However, in the first four months of 2014, there is significantly more activity in Asia.

M&A Transactions by Geography – Target

Photonics & Vertical Markets Served

January – April 2014

M&A Transactions by Geography – Buyer

Photonics & Vertical Markets Served

January – April 2014

More than 25% of transactions represent buyers acquiring targets outside their geographical region.

Most Active Buyers

Financial buyers in Korea are by far the most active – acquiring small and middle market optics, laser, and materials companies. Another 8 strategic buyers, including Stratys, Phillips, and Carl Zeiss, acquire two entities each.

Following Thermo Fisher’s acquisition of Life Technologies, the largest transactions thus far in 2014 are: Corning’s acquisition from Samsung of Korea based supplier of inorganic materials and TFT-LCD glass substrates for displays and solar devices, and thermochromic coated glass/solar light control glass; The Carlyle Group’s acquisition of Johnson & Johnson’s Ortho-Clinical Diagnostics; and Facebook’s acquisition of Oculus VR, a manufacturer of wearable immersive virtual reality technology.

The Transactions

Follow this link to transaction detail. <2014 Jan to April Photonics M&A Transactions>