Photonics Enables World Change in Product Development & Manufacturing

Additive Manufacturing, also known as 3D Printing, is an innovation grounded in photonics. It is a process for making a physical object from a 3D digital model, typically by laying down many successive thin layers of a material. The technology is diffusing from prototyping to large scale manufacturing of final parts. Today, early adopters including GE, Siemens, Google/Motorola, and Boeing are 3D printing intricate, high mix, low volume, and weight-sensitive final parts.

With access to private and public capital, market leaders in Additive Manufacturing cross the chasm to rapid growth via acquisitions and strategic partnerships. In the last 24 months, more than $200million and $1billion in private placements and public offerings go to work commercializing technology and scaling development stage and high growth Additive Manufacturing businesses.

The 3D Printing Market

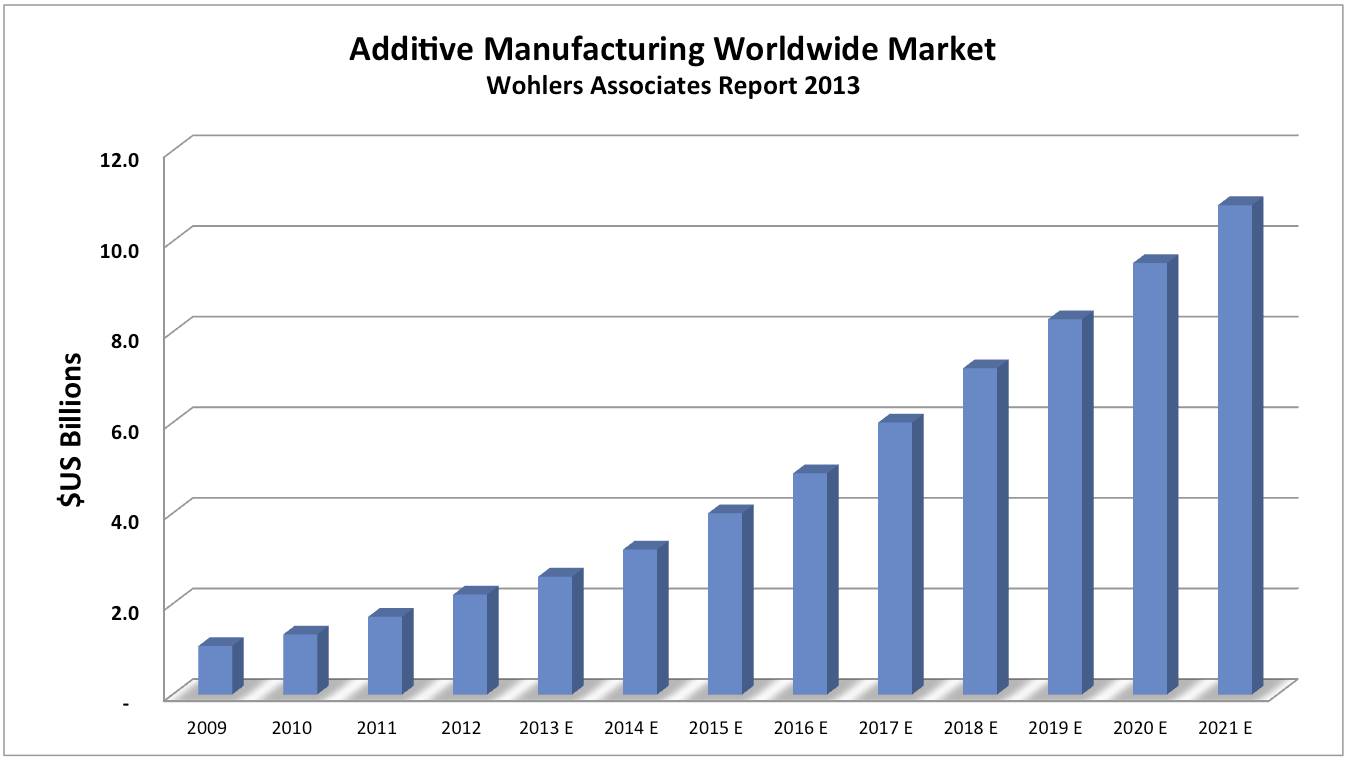

According to Wohlers Associates, the market for 3D Printing in 2012, consisting of all products and services worldwide, grows 28.6% (CAGR) to $2.2billion. The compounded average annual growth (CAGR) of the industry over the past 25 years is an impressive 25.4%.

Growth of the low-cost (< $5,000) “personal” 3D printer market segment averages 346% per year from 2008 through 2011. In 2012, the increase cools to an estimated 46.3%. Most machines are sold to hobbyists and educational institutions.

The 3D printing industry is expected to continue strong double-digit growth over the next several years. By 2017 and 2021, Wohlers Associates forecasts sales of products and services to approach $6.0 and $10.8billion worldwide.

Prototyping vs. Mainstream Manufacturing

Additive Manufacturing is most often used to quickly create detailed prototypes. As 3D printers become more and more affordable, rapid prototyping is done in the office, no longer requiring manufacturing floor space and resources.

According to Wohlers Report 2013, final part production (vs. prototype production) rose to 28.3% of the $2.2billion spent in 2012 on 3D printing products and services worldwide. In 2003, it represented only 3.9% of revenues. The production of parts for final products is forecast to far surpass prototyping and the opportunity for more commercial production activity from Additive Manufacturing is immense.

The use of Additive Manufacturing in final parts production is growing in several diverse market segments including dental work, orthopedic implants, and jewelry. GE Aviation will 3D print 40,000 fuel nozzles annually for its next generation LEAP turbo fan engine. Boeing uses Laser Sintering extensively to produce environmental control system ducting for directing the flow of air on military and commercial aircraft. Siemens expects to produce more than 100 unique individual metal replacement parts for gas turbine repairs using Additive Manufacturing. Google and Motorola are collaborating with market leader, 3D Systems, to develop a high-speed continuous 3D printing production platform for its next generation smartphone.

The Market Leaders

There are hundreds of companies worldwide providing printers, scanners, materials, software, integrated systems, contract manufacturing services, and content for Additive Manufacturing.

The $3billion market, however, is dominated by a handful of players.

Market Share by 3D Printer Units

Mergers & Acquisitions, Private Placements, and Public Offerings

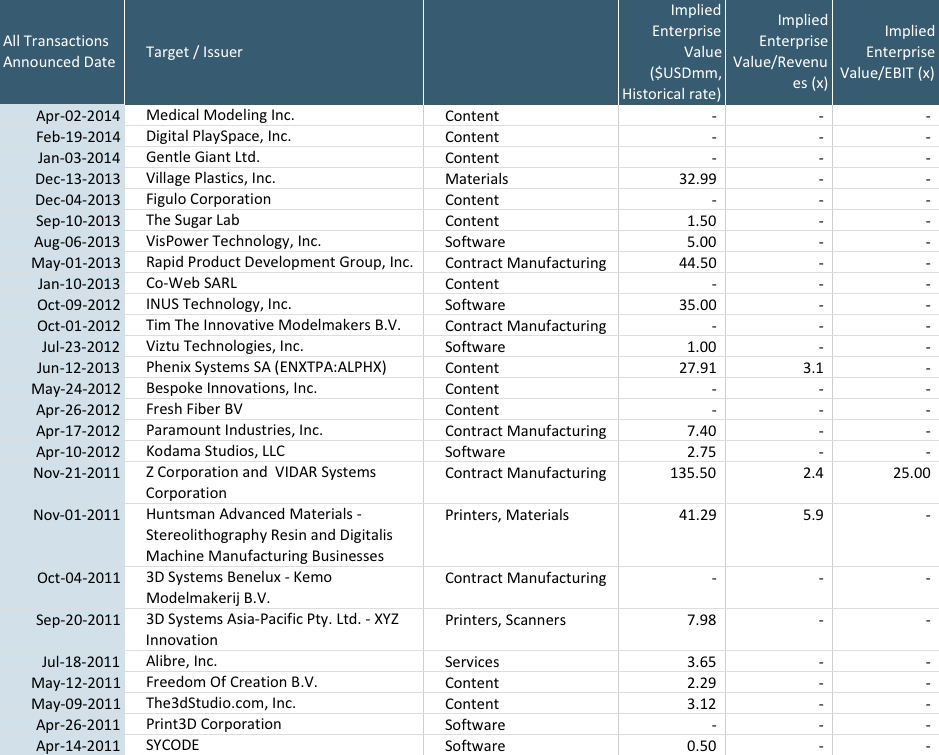

Transactions are researched for the last three years ending April 14, 2014. Values are in $US at historical rates of exchange. Follow this link to transaction detail. <Additive Manufacturing Transactions April 15 2012 to 2014>

Mergers & Acquisitions

With access to private and public capital, market leaders in Additive Manufacturing cross the chasm to rapid growth via acquisitions and strategic partnerships. Valuation statistics based on researched transactions are summarized below.

The most active buyer is 3D Systems, acquiring 40 companies. They include 3D printing systems companies employing six unique printing technologies – as well as providers of 3D scanners, materials, software, rapid prototyping and contact manufacturing services. Unlike its closest competitor, Stratasys, 3D Systems is aggressively and opportunistically acquiring companies that provide 3D printed products to end-user markets (“content”), such as medical devices, toys, art, consumer electronic gadgets, lighting, and housewares.

Stratasys employs two unique printint technologies, including those acquired from formerly private equity owned Solidscape, Objet, and MakerBot. This month, Stratasys extends horizontally to acquire rapid prototyping and contract manufacturing services companies, Solid Concepts and Harvest Technologies. Summarized below are valuations, including strategic premiums, paid by Stratasys.

Private Placements and Public Offerings

More than $200million in 35 private placements go to work commercializing technology and scaling development stage and high growth additive manufacturing businesses. In the past three years, market leaders, 3D Systems Corp., Stratasys Ltd., Voxeljet AG, Arcam AB, and Materialise NV issue Public Offerings totaling $1.2billion. The majority of financings fuel R&D and capital intensive providers of 3D printer/scanner hardware, materials, and contract manufacturing services.

Of the countless entrepreneurial opportunities, many do not require significant up-front investment. Service and software providers that facilitate content creation require very little investment to start-up and most often can grow on cash flows. They do not bear the high costs and inherent high risk of hardware, materials, and process development related R&D.

Changing the World

As prices decrease and applications for Additive Manufacturing diffuse, the implications are enormous. Goods will be manufactured close to their point of purchase or consumption – even at the household level. Imagine buying raw materials and software files. Goods will be infinitely more customized. This means a switch from centralized factories to local production with higher unit costs but no shipping and inventory costs.

Supply, manufacturing, and retailing strategies and operations will change to adapt. China’s deeply engrained pro-producer mass-manufacturing model would be a competitive disadvantage. Per Richard D’Aveni, Professor of Dartmouth’s Tuck School of Business, “The great transfer of wealth and jobs to the East over the past two decades may have seemed a decisive tipping point. But this new technology will change again how the world leans.”

Countless Opportunities Across the Value Chain

Along with the countless opportunities for growth and healthy exits for 3D printing hardware companies, systems integrators, software providers, and contract manufacturers, are tremendous opportunities for manufacturers of lasers, light sources, scanners, optomechanical positioning, optics, and digital filters. Next generation 3D printers and scanners in development today are improving processing speed, post processing, structural integrity, material selection, and capital equipment costs. This is fertile ground for established and emerging photonics companies to accelerate the change that is happening in the world of manufacturing today.

The Technologies

Additive Manufacturing solutions process successive layers of material to produce a 3D object. The object is specified by a 3D Computer Aided Design (CAD) model. 3D printer software transforms the virtual 3D model into a series of layers suitable for printing the object.

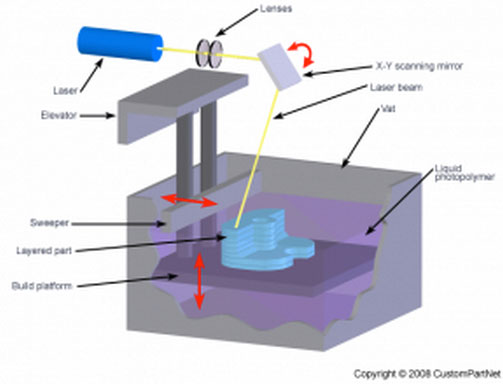

Stereolithography (SLA)

SLA is the most widely used rapid prototyping technology that creates 3D objects by “printing” thin layers of an ultraviolet curable material. It can produce highly accurate and detailed polymer parts. It uses a low-power, highly focused UV laser to trace out successive cross-sections of a three-dimensional object in a vat of liquid photosensitive polymer.

SLA technology is incorporated into 3D printers supplied by market leader, 3D Systems Corporation.

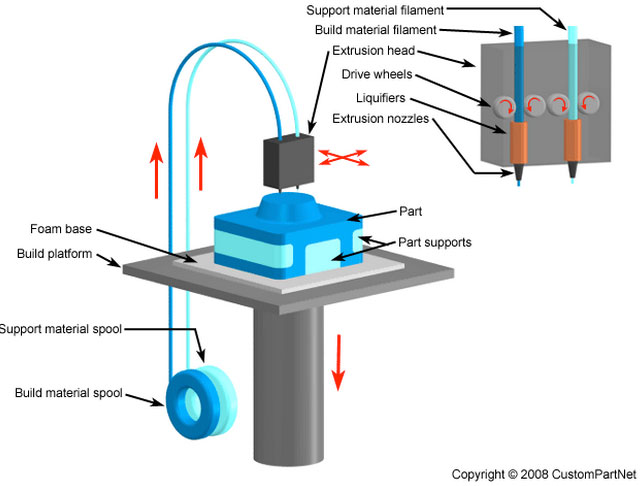

Fused Deposition Modeling (FDM)

FDM works on an “additive” principle by laying down material in layers. A plastic filament or metal wire is unwound from a coil and supplies material to an extrusion nozzle that can turn the flow on and off. The nozzle is heated to melt the material and can be moved in both horizontal and vertical directions by a numerically controlled mechanism, directly controlled by a computer-aided manufacturing (CAM) software package. The model or part is produced by extruding small beads of thermoplastic material to form layers as the material hardens immediately after extrusion from the nozzle.

FDM technology is incorporated into 3D printers supplied by market leader, Stratasys Ltd.

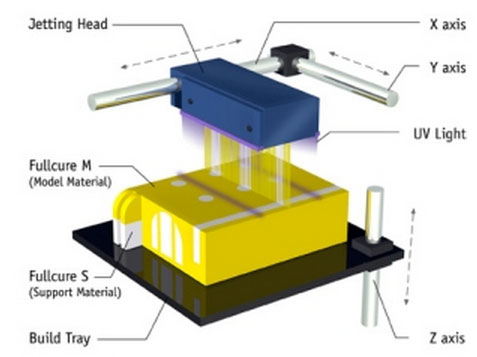

Jetting

Jetting is similar to inkjet document printing. Instead of jetting drops of ink on paper, layers of liquid photopolymer are jetted on a build tray and cured with UV light. The layers build up to create a 3D model. Fully cured models are used immediately without additional post-curing. Along with the selected model materials, the 3D Printer also jets a gel-like support material that is designed to uphold complicated geometries and is easily removed.

Jetting has many advantages including quality, high speed, precision, and selection of a wide range of materials. Based on its jetting technology, Stratasys (Objet) can uniquely combine different 3D printing materials within the same 3D printed model, in the same print job. Jetting technology can create 16micron layers with accuracy up to 0.1 mm for smooth surfaces, thin walls, and complex geometries. It uniquely supports a range of materials from rubber to rigid and from transparent to opaque.

Jetting technology is incorporated into 3D printers supplied by market leaders, Stratasys Ltd. and 3D Systems Corporation.

Powder Based Jetting

As with many other rapid prototyping processes, the part is built up from many thin cross sections of the 3D model. An inkjet-like printing head moves across a bed of powder, selectively depositing a liquid binding material in the shape of the section. A fresh layer of powder is spread across the top of the model, and the process is repeated. Photopolymerization is cured with UV light. When the model is complete, unbound powder is automatically removed.

Parts can be built at a rate of approximately 1 vertical inch per hour. This technology accommodates full color, by varying the color of the binding liquid applied by the printing head at any location.

Powder based technology is incorporated into 3D printers supplied by market leaders, The ExOne Company, Voxeljet AG, and 3D Systems Corporation (ZCorp).

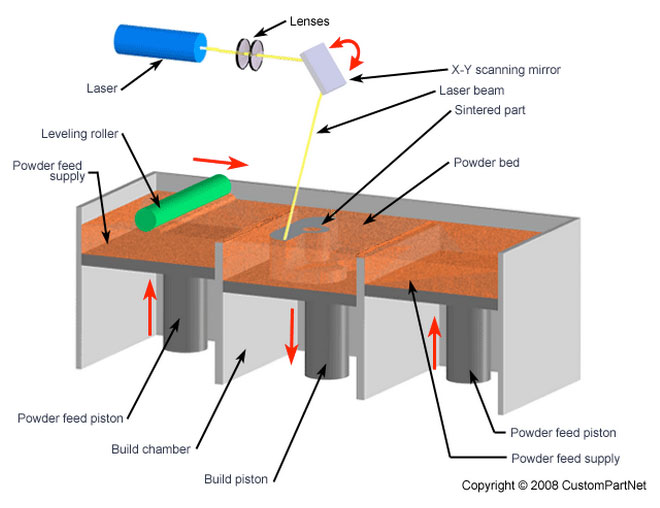

Selective Laser Sintering (SLS)

The basic concept of SLS is similar to that of SLA. It uses a moving laser beam to trace and selectively sinter powdered polymer and/or metal composite materials into successive cross-sections of a 3D part. The parts are built upon a platform that adjusts in height equal to the thickness of the layer being built. Additional powder is deposited on top of each solidified layer and sintered. This powder is rolled onto the platform from a bin before building the layer. The powder is maintained at an elevated temperature so that it fuses on exposure to the laser.

Unlike some other Additive Manufacturing processes, such as stereolithography (SLA) and fused deposition modeling (FDM), SLS does not require support structures due to the fact that the part being constructed is surrounded by unsintered powder at all times. This allows for the construction of geometries not achievable with other technologies.

SLS technology is incorporated into 3D printers supplied by market leaders, Renishaw plc, EOS GmbH, and SLM Solutions GmbH

Direct Metal Laser Sintering (DMLS)

With DMLS, metal powder with diameters of approximately 20 microns and free of binder or fluxing agent, is melted when scanned with a high power laser to build a part with properties of the original material. Eliminating the polymer binder avoids the burn-off and infiltration steps, and produces a 95% dense steel part compared to roughly 70% density with Selective Laser Sintering (SLS).

An additional benefit of DMLS compared to SLS is higher detail resolution due to thinner layers, enabled by a smaller powder diameter. This capability allows for more intricate shapes. Material options include alloy steel, stainless steel, tool steel, aluminum, bronze, cobalt-chrome, and titanium. In addition to functional prototypes, DMLS is often used to produce tooling, medical implants, and aerospace parts for high heat applications.

DMLS technology is incorporated into 3D printers supplied by market leaders, EOS GmbH, and 3D Systems Corporation.

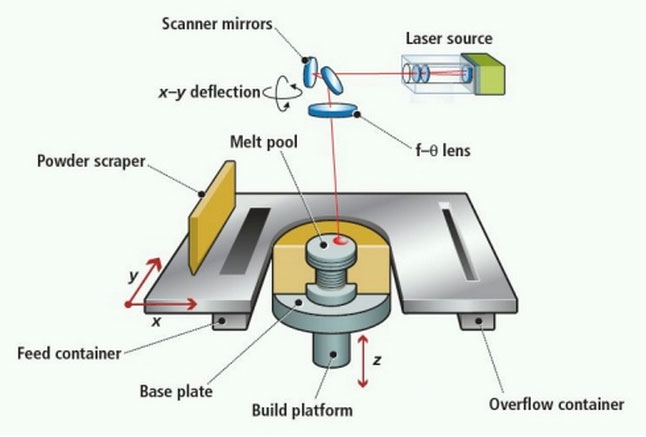

Selective Laser Melting (SLM)

SLM is an Additive Manufacturing method that uses high power lasers to melt metallic powders together to shape the product from 3D CAD data. Renishaw 3D Printers incorporate a high power fiber laser to fuse metal powders. The re-coater sweeps a layer of fine material powder to prepare for the laser to fuse according to the 2D cross section of each layer under a tightly controlled inert atmosphere. When the part is complete, it is heat treated and post processed. Typical applications are functional testing of production quality prototypes, manufacturing of organic or highly complex geometries, and low volume manufacturing of complex metal parts in specialty materials.

SLM technology is incorporated into 3D printers supplied by market leader, Renishaw plc.

Electron Beam Melting (EBM)

Similar to Selective Laser Melting (SLM), but using an electron beam as its power source, Electron Beam Melting (EBM) technology manufactures parts by melting metal powder layer by layer in a high vacuum.

Laser melting has improved significantly over the past several years, but it still produces parts with micro-voids and heat-induced stress. EBM has emerged as a higher quality alternative. The very high-energy density enables it to produce fully dense, void-free parts with greater load-bearing characteristics. It is increasingly being used in the manufacture and repair of turbine blades.

EBM technology is incorporated into 3D printers supplied by market leader, Arcom AB.

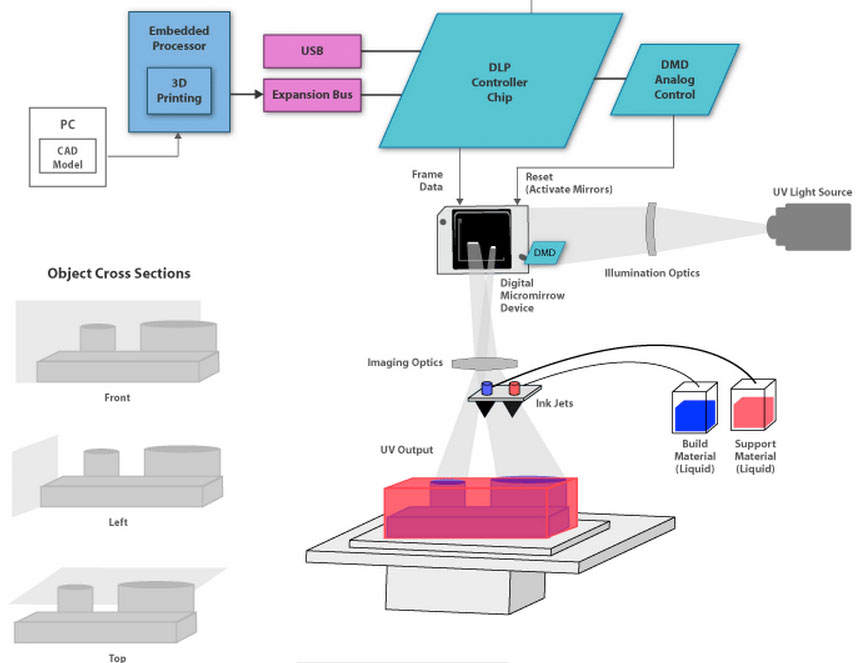

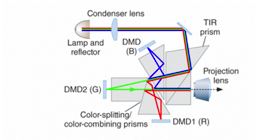

Digital Light Processing (DLP)

DLP technology can be applied to digital exposure and laser sintering methods. Digital exposure is represented below. The 3D object is constructed by laying down successive thin horizontal cross-sections or layers of an ultraviolet (UV) curable liquid photopolymer resin. For each layer, the UV light image from the Texas Instruments DLP® Digital Micromirror Device (DMD) creates a pattern that hardens the polymer resin where it is exposed to the light.

The cross-section pattern is produced by the individual mirrors that correspond to each pixel on the current layer. This pattern projects through an imaging lens onto the surface of the UV curable liquid photopolymer resin, curing or hardening it where the pixels are on.

As depicted, one resin is the build material and the second is material to support overhanging features and thin vertical walls during construction. The support material is later removed by heat or dissolved with a solvent or water. These layers fuse automatically and the process repeats one layer at a time until the model is built. Cure rates are possible under 0.2 seconds per layer. Layer thickness typically ranges from 1um to 250um based upon the resin and wavelength of the UV light used.

DLP technology is incorporated into 3D printers supplied by market leader, envisionTEC, GmbH.