Realizing Higher Average Valuations than All Other Sectors

2015 was an extraordinary year for M&A. There were 16,837 transactions worth $4.3trillion announced globally. Although a drop in volume from 17,397 transactions in 2014, the total value rose 31% from 2014, breaking 2014’s previous record of $3.3trillion. Compared to the M&A market as a whole, the photonics industry and vertical markets employing photonics technologies as core differentiators realize higher average valuation multiples than other sectors.

Middle market companies employing photonics to serve a wide breadth of markets, such as Display, Medical Diagnostics, Ophthalmics and Solar are realizing very high valuations. Asia based middle market companies realizing premium valuations from strategic buyers are also driving-up average Enterprise Value multiples.

Leading in Enterprise Value to Revenue multiples in Display are: Chunghwa Picture Tubes, manufacturer of liquid crystal and flat panel displays (108x); IRICO Display Devices, provider of LCD and OLED components (62x); Beijing Baofeng Mojing Technology, manufacturer of virtual reality headsets (42x). Employing Biophotonics and leading the pack are: DioGenix, molecular diagnostics company providing DNA sequencing assays to identify patients with multiple sclerosis (62x); and InSight Vision, ophthalmic company developing proprietary drug delivery technology (13x).

The Transactions

M&A transactions are researched with closing or announce dates from January 1 to December 31, 2015. Transactions volumes, values, geographies, and market segments are analyzed. Values are in $US at historical rates of exchange. Implied Enterprise Value is defined as the total consideration to shareholders (adjusted for % acquired) plus earnouts plus rights/warrants/options plus size adjustment plus net assumed liabilities.

Follow links at the end of this article for transaction detail.

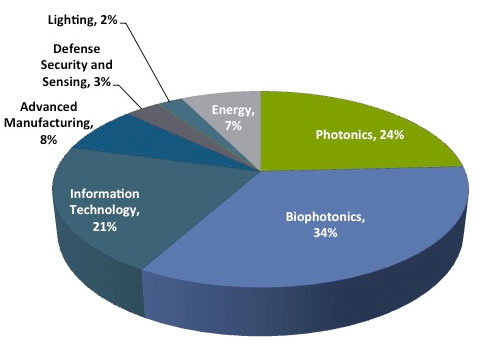

M&A Transaction Size

Photonics & Vertical Markets Served

2015

Activity

The Materials and Coatings, Communications, Medical Devices and Solar segments see the most activity in volume of transactions.

M&A Transaction Volume

Photonics & Vertical Markets Served

2015

In 2015, the total and average Enterprise Value of the 564 transactions reporting financial data were $391billion and $718million – compared to $190billion and $462million in all of 2014 respectively.

M&A Transaction Value

Photonics & Vertical Markets Served

2015

Photonics Core Technology Companies

The largest acquisition of core photonics technology announced is the acquisition of OmniVision Technologies (CA), a provider of semiconductor image-sensor devices with integrated wafer-level optics used in various consumer and commercial mass-market applications for $1.9billion. OmniVision is sold by US private equity firms to three China and Hong Kong based private equity firms.

Recent advances in commercially available materials and their related photonics technologies are driving innovation in lighting, life sciences, IT, energy, and construction. 22% of the total M&A market value is in Materials and Coatings – suppliers of fundamental materials such as rare earths, organic LED materials, dielectric optical coatings, semiconductors, nanoparticles, sapphire and display glasses.

Small and Middle Market

47% of researched transactions disclosed the transaction value. Of those disclosed and consistent with previous four years, 78% are small market (<$5M), micro middle market ($5 to $25M), and small/middle market ($25 to $100M) transactions.

Since 2010, the lower and middle of the M&A middle markets remain robust. These researched transactions are consistent with that market as a whole. However, uniquely, in the Photonics sector and the vertical market segments enabled by photonics, strategic buyers are acquiring orders of magnitude smaller businesses providing products that are highly differentiated with strong intellectual property positions.

M&A Transaction Size

Photonics & Vertical Markets Served

2015

Strategic vs. Financial on Buy and Sell Side

Like 2012 through 2014, the vast majority of transactions by volume and value are strategic. However, financial buyers and sellers are consistently more active since 2012 – financial buyers up to 20% from 3% of transactions and financial sellers up to 21% from 12%. Considering strategic buyers are more active in 2014 and 2015, this is a seller’s market with higher strategic premiums in valuations for both strategic and financial buyers.

Valuations

For researched market segments, the average and median of reported Enterprise Value to EBIT, EBITDA and Revenue multiples in 2015 and 2014 trend higher since 2012 and 2013 – especially multiples of EBIT and EBITDA. Implied Enterprise Value includes implied equity value, earn-out and contingent payments, rights, warrants, options, and net assumed liabilities adjusted for size.

Photonics and Markets Served

Photonics

The Therapeutics (Biohotonics), Medical Imaging (Biophotonics), and Display (Information Technology) segments realize high average multiples of Enterprise Value to Revenue due to strategic acquisitions of lower middle market companies with strong IP portfolios serving high growth markets like point-of-care medical devices and consumer electronics.

High average multiples of Enterprise Value to EBITDA for 100% equity transactions were realized by Volcano, a manufacturer of precision guided therapy medical devices (76x EBITDA); Sutran, a provider of real time data collection for environmental monitoring (56x EBITDA); and Transmode, a provider of passive optical networking telecommunications gear (30x EBITDA).

Few transactions report financials, because buyers are not required if a transaction does not have material near term impact on their financial statements. M&A transaction data is highly relevant, however, to understand market dynamics and buyer behavior.

Geography

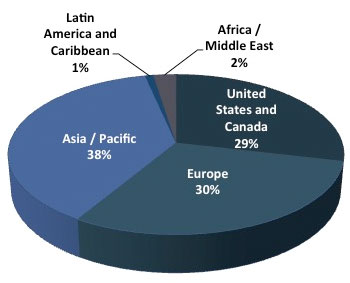

Historically, the United States and Canada, as a geographical region, experience the most buy and sell side activity. This trend is changing. In 2015, we see a much higher concentration of targets in Asia and Europe and of buyers in Asia.

M&A Transactions by Geography – Target

Photonics & Vertical Markets Served

2015

M&A Transactions by Geography – Buyer

Photonics & Vertical Markets Served

2015

Down from more than 25% in 2014, 18% of transactions represent buyers acquiring targets outside their geographical region.

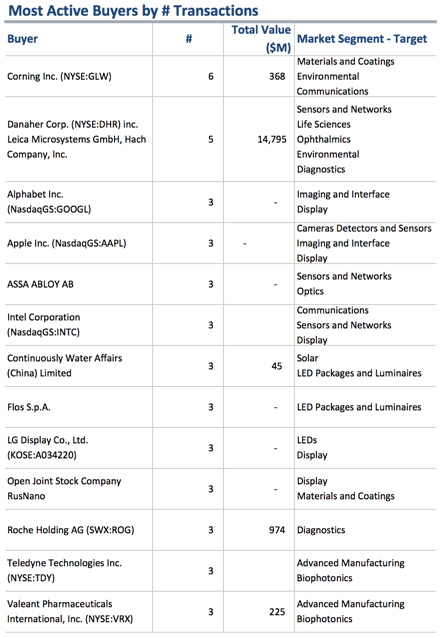

Most Active Buyers

Strategic buyers are by far the most active – acquiring small and middle market companies across a wide breadth of photonic technology enabled market segments. Consistent with previous years, Corning, Danaher and Intel are very active buyers. Unlike in 2014, there are not a relatively large number of acquisitions per strategic buyer.

Although most diversified market leaders in Photonics are not acquisitive at all in 2015, there are four atypically large transactions in Photonics.

- E. I. du Pont de Nemours and Company (NYSE:DD) by The Dow Chemical Company (NYSE:DOW) for 72,835mm

- OmniVision Technologies, Inc. (NasdaqGS:OVTI) by CITIC Capital Partners; Gold Stone Investment Co., Ltd.; Hua Capital Management Ltd. for $1,900mm

- Mirion Technologies, Inc. by Charterhouse Capital Partners LLP for $750mm

- OCI Materials Co., Ltd. (KOSDAQ:A036490) by SK Holdings Co. Ltd. for $418mm

The Transactions

Follow this link to transaction detail for Photonics and Markets Served. <Download 2015 Photonics M&A Transaction Detail>