Mergers & Acquisitions in Photonics | First Half 2024

There remains a lot of uncertainty in the global M&A market as a whole in the first half of 2024. Deal volume is down and total deal value is flat compared to the record lows of 2023. However, M&A activity for targets employing photonics technology appears to be on a healthy upward trajectory.

High interest rates, lower valuations and geopolitical instability are show-stoppers for many buyers and sellers, while fueling the strategic need for M&A to grow stronger, creating pent-up demand.

Why be optimistic the pent-up demand will let loose in the near term when macroeconomic trends are not forecast to change? Organic revenue growth is difficult to achieve in today’s low growth economies. Further, faced with technological disruptions and labor shortages, corporations can not only survive, but succeed by acquiring key competitive capabilities, talent and technology or by divesting non-core assets today. Also, after a long dry period, private equity funds need to divest portfolio companies to generate investor distributions and attract new investment capital.

Why be even more bullish on targets with core photonics technology? The explosion of Artificial Intelligence applications and cybersecurity threats create an insatiable demand for computing that only optical communications and in the future, quantum computing can fill. Geopolitical instability is fueling game-changing, photonics enabled solutions in drones and counter-drone technology; Laser Directed Energy Weapons (LDEW); military robots; 3D printing of munitions; and Counter Communications Systems (CCS) for electronic warfare. In manufacturing and service industries alike, photonics enabled automation and robotics solutions are alleviating labor shortages and reducing costs as inflation remains stubborn.

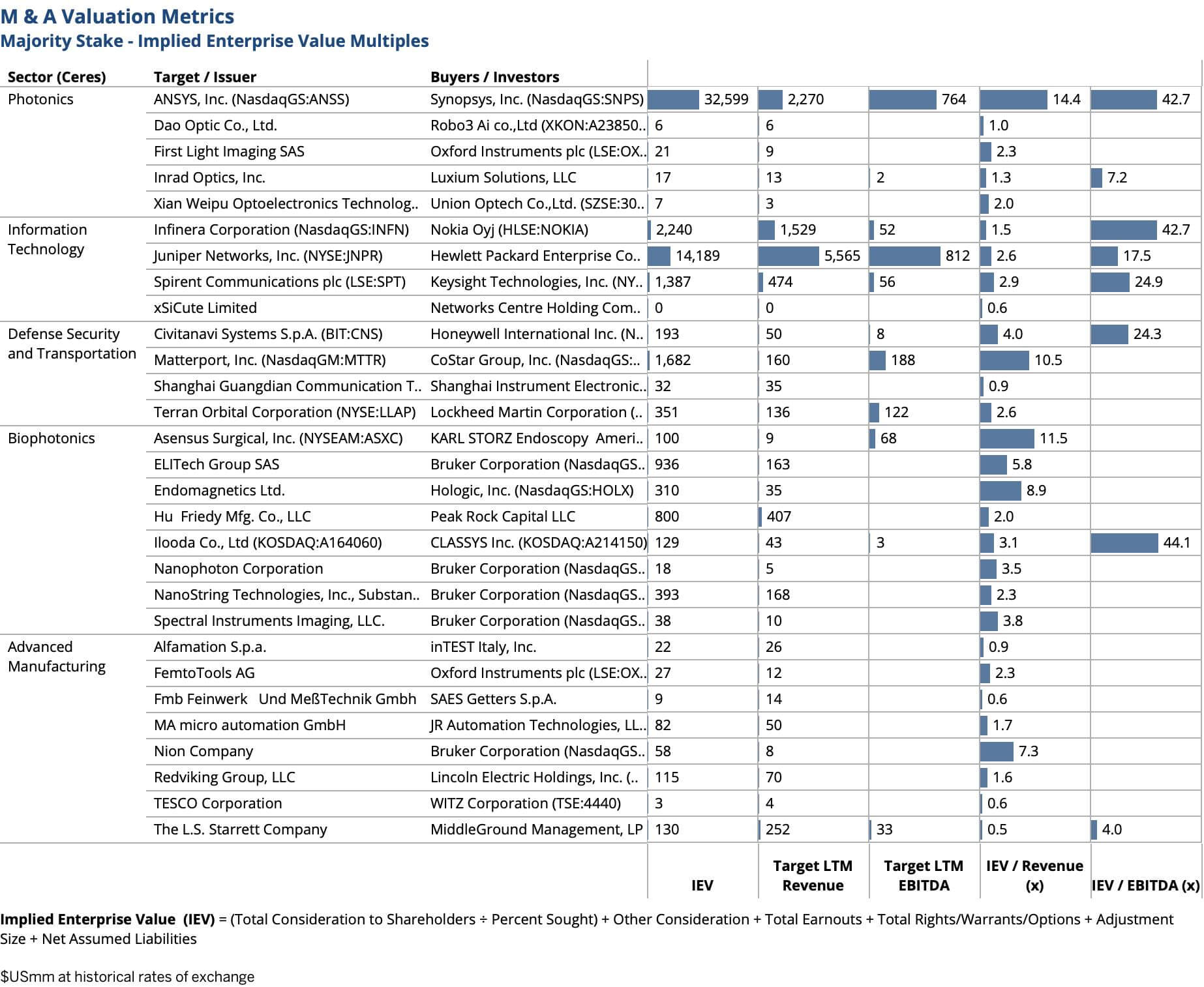

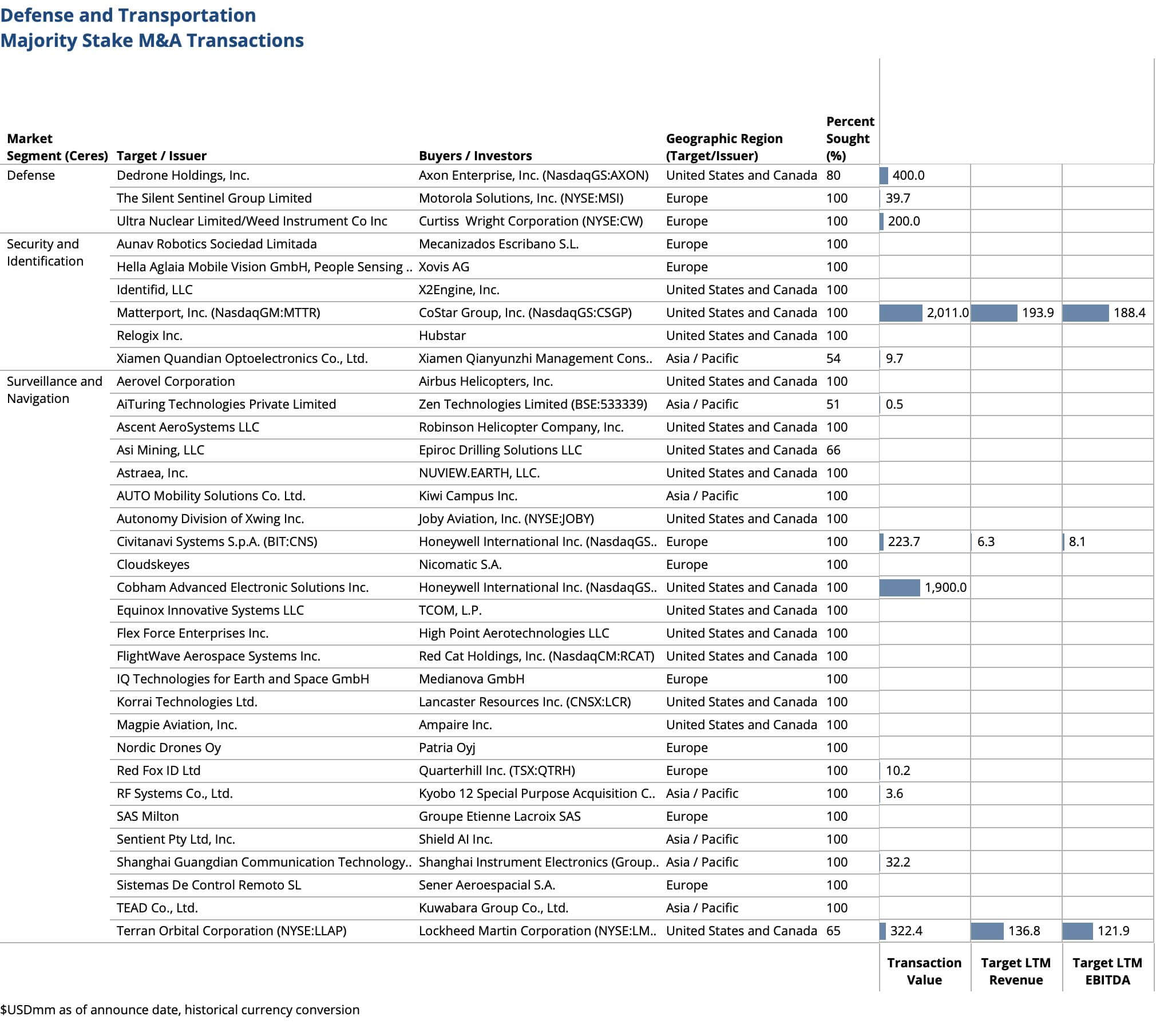

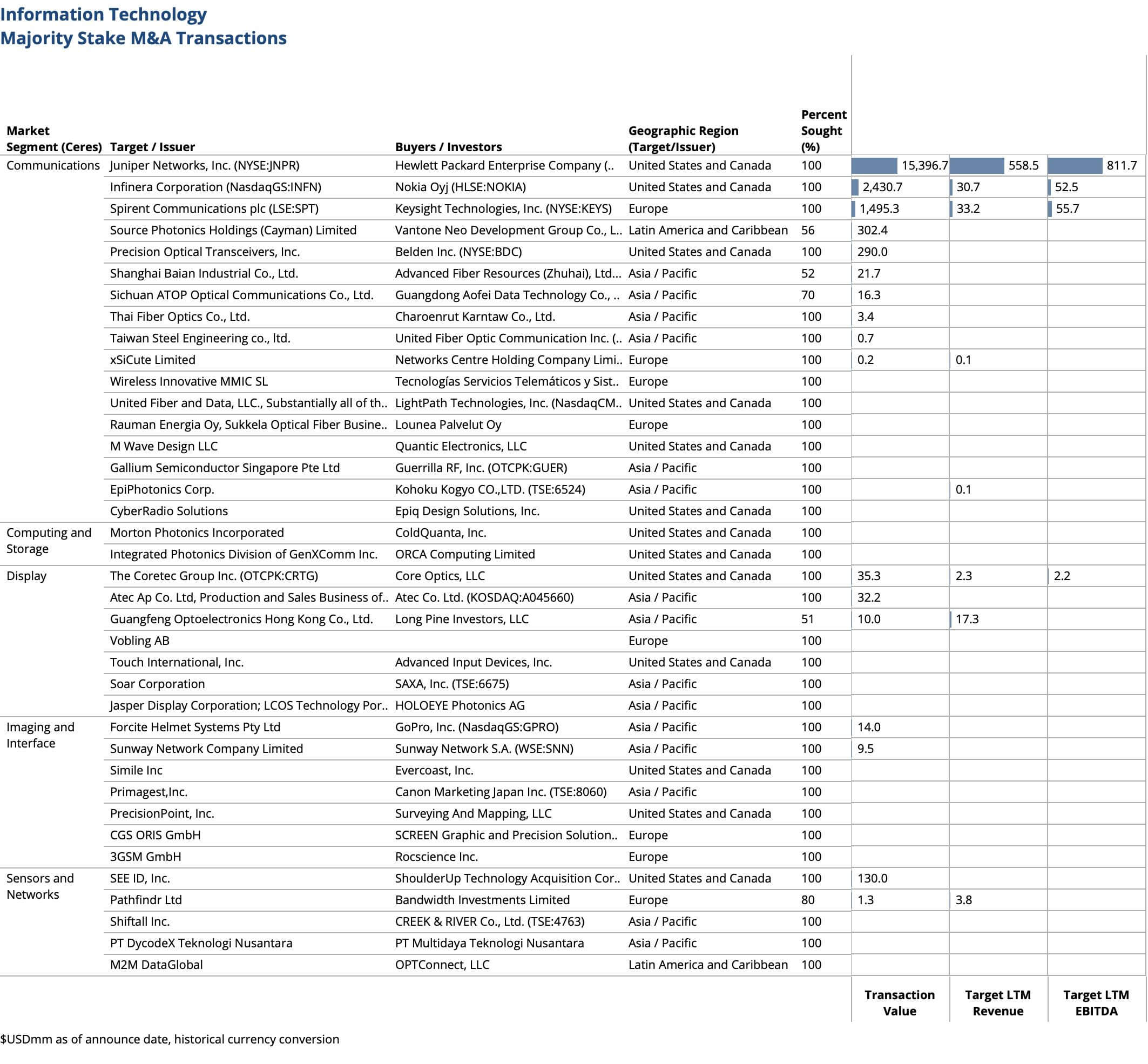

After a very slow start in the first quarter of 2024, the volume of transactions for photonics targets is now tracking 30% higher than 2023. Total deal value of $67billion is tracking higher than 2021 peak with the announcement of large deals, including Synopsys, Inc. $33B acquisition of ANSYS, Inc., a supplier of engineering simulation software and services; Hewlett Packard $15B acquisition of Juniper Networks, Inc., a supplier of optical data communications networking equipment; Nokia Oyj $2.4B acquisition of Infinera Corporation, supplier of optical access to long haul networking gear; and CoStar Group $2.0B acquisition of Matterport, Inc., pioneer of LiDAR and AI based digital twin technology.

The Transactions

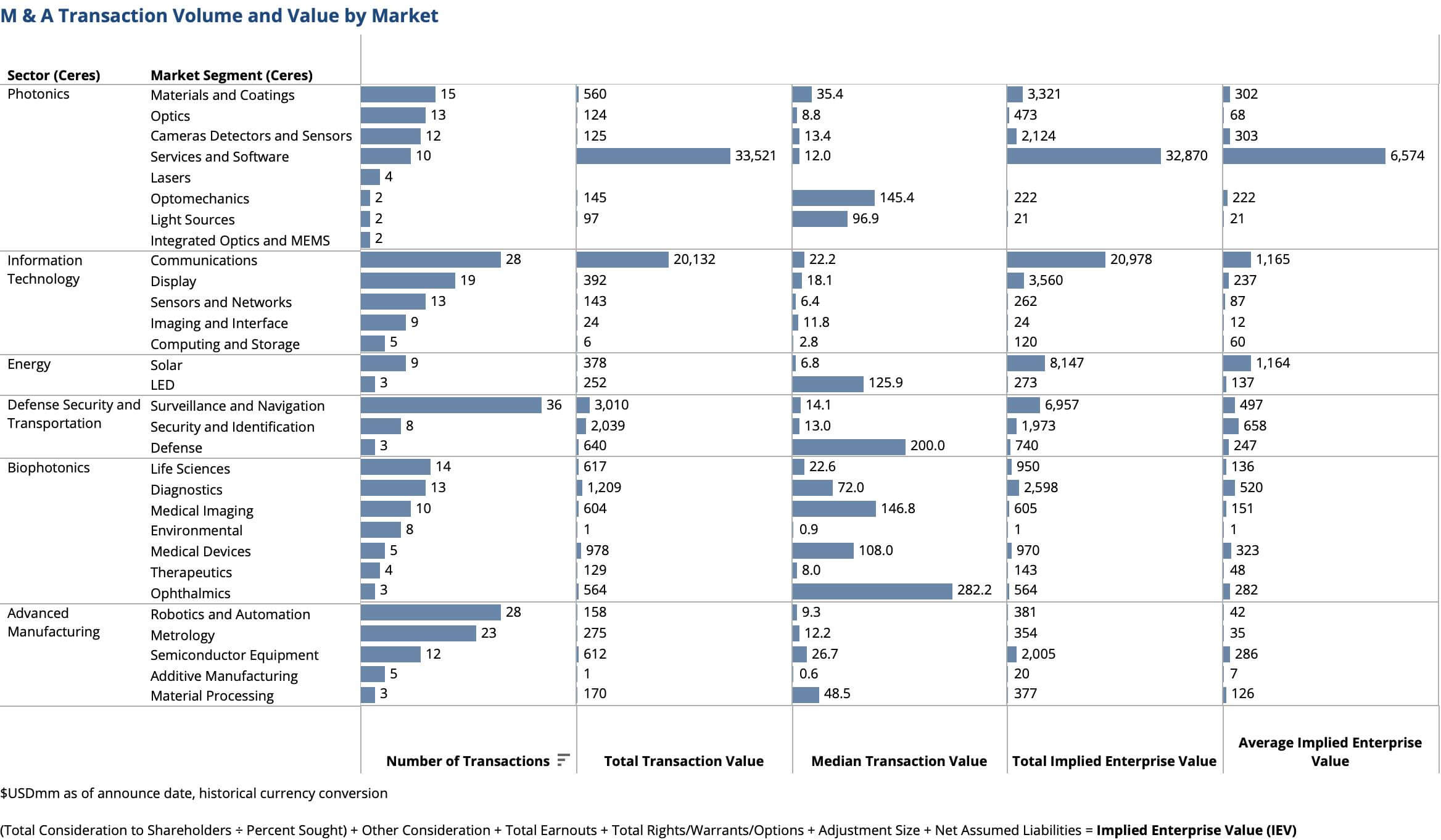

M&A transactions are researched with announce dates from January 1 to June 30, 2024. Activity and valuations are analyzed by market segments. Values are in $US at historical rates of exchange. Implied Enterprise Value (IEV) is defined as the total consideration to shareholders (adjusted for % acquired) plus earn-outs plus rights/warrants/options plus size adjustment plus net assumed liabilities.

Inconsistent with previous years, Communications (Information Technology) and the Surveillance and Navigation (Defense Security and Transportation) see the most activity in first half. The high level of activity and relatively low total value in Surveillance and Navigation is evidence of a continued high concentration of capabilities deals. While the high total value and low level of activity in Communications is evidence of consolidation.

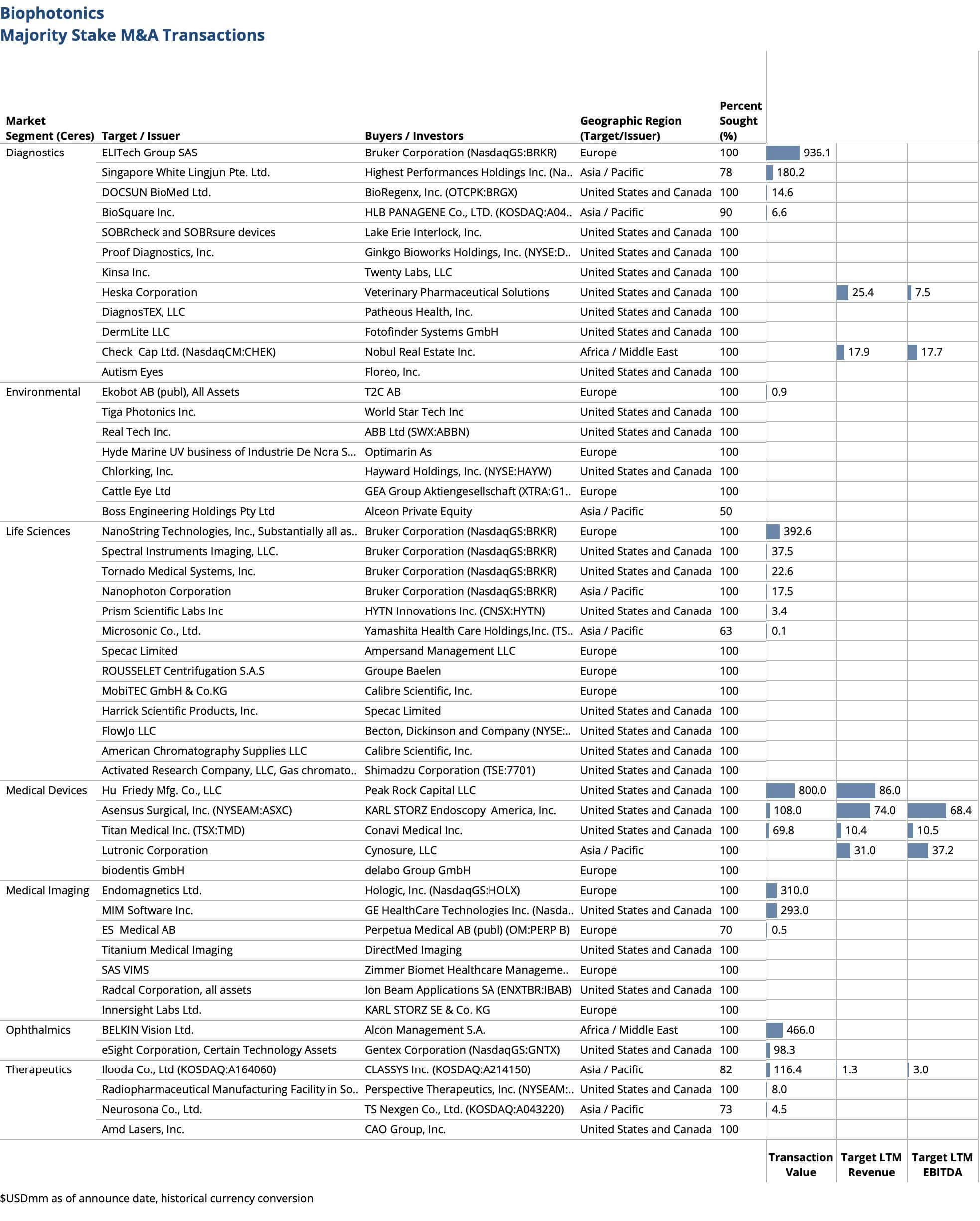

Inconsistent with previous years, Biophotonics does not see the most activity and highest total value of all photonics enabled sectors this quarter. This is inherent to today’s market conditions in medical devices and diagnostics.

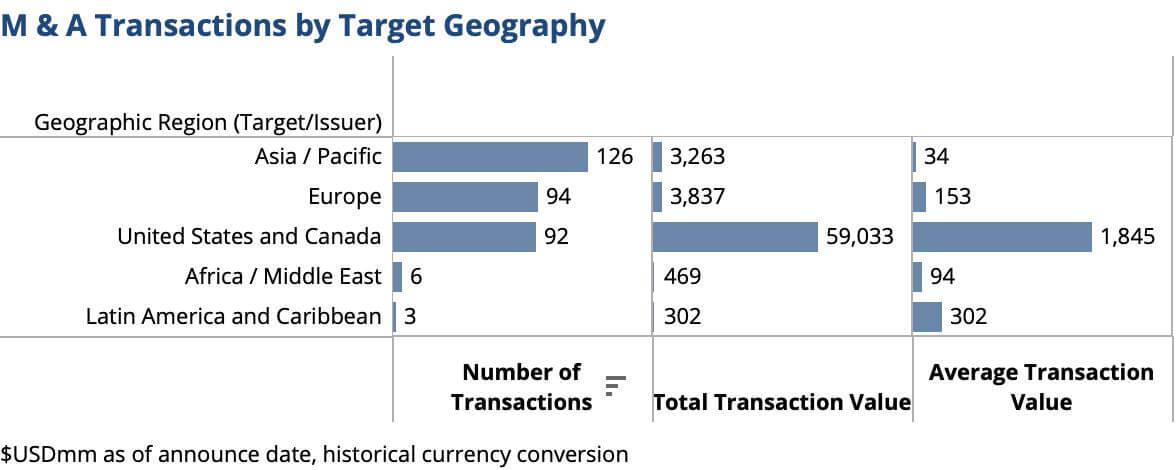

Geographically, in line with 2023, the first half 2024 sees target M&A activity in Asia and Pacific region out pacing both Unites States/Canada and Europe.

The Valuations

In the M&A market as a whole, strategic deals trade at the highest multiples in history across the board in 2021 with the decreasing valuations in 2023 continuing into the first half 2024. Many generalist analysts predict valuations to stabilize here with a new normal of higher interest rates and geopolitical instability. Based on researched transactions for targets with photonics technology, 2021 was also a banner year, but in contrast with the M&A market as a whole, strategic deals continue to trade relatively high for photonics targets.

Very few transactions report target financials. Of the researched transactions for majority stake, 32 buyers report Implied Enterprise Value (IEV) multiples for majority stake.

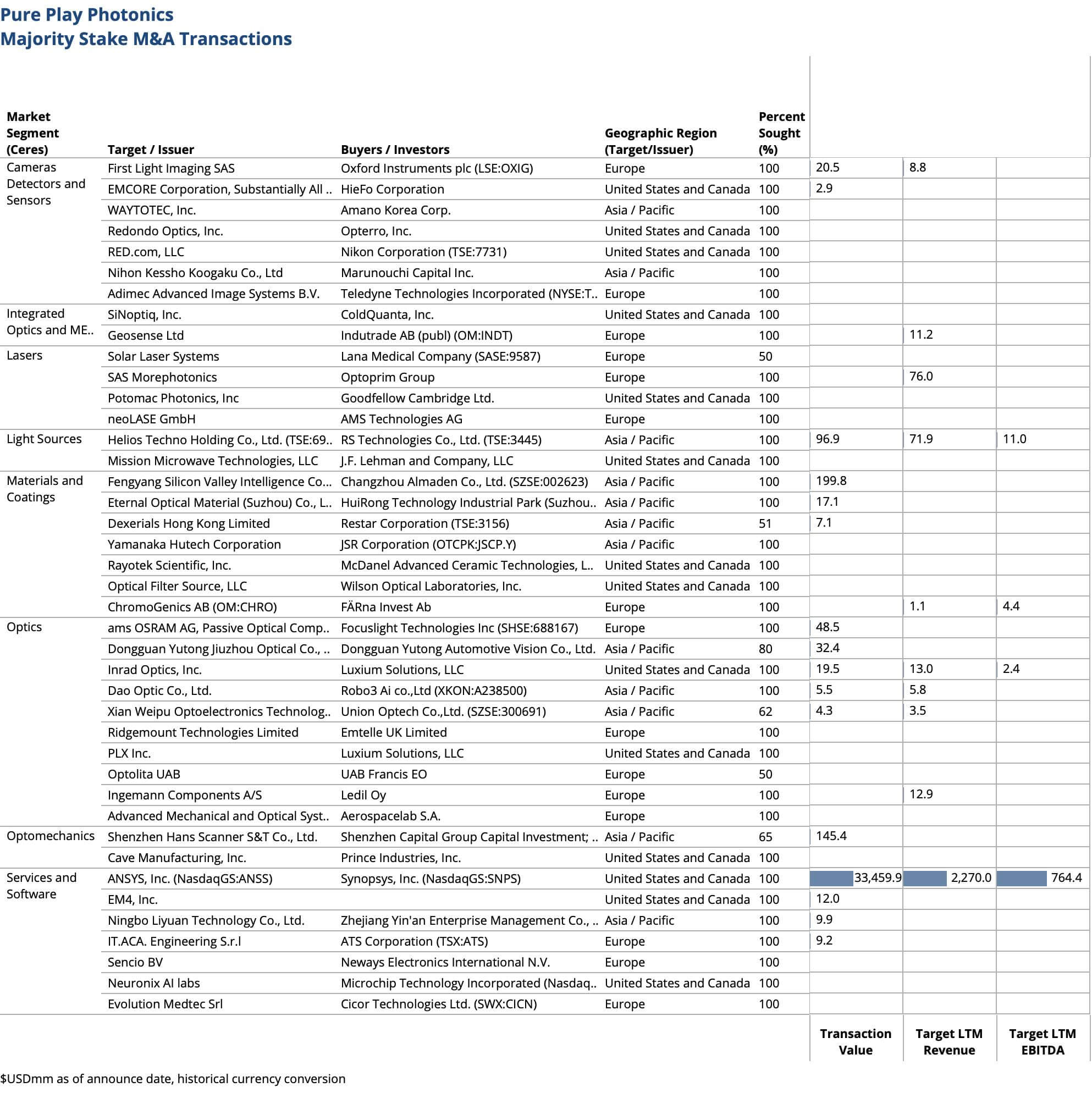

The Pure-Play Photonics Targets

Most pure-play photonics market leaders are not acquisitive in 2023 and 2024. However, the total and average value, as well as number of transactions are tracking toward 2021 and 2022 highs. In addition to handful of small strategic acquisitions of capabilities, product lines and technical talent, there is a material increase in pure-play photonic targets acquired for vertical integration.

The Targets with Core Photonics Technology

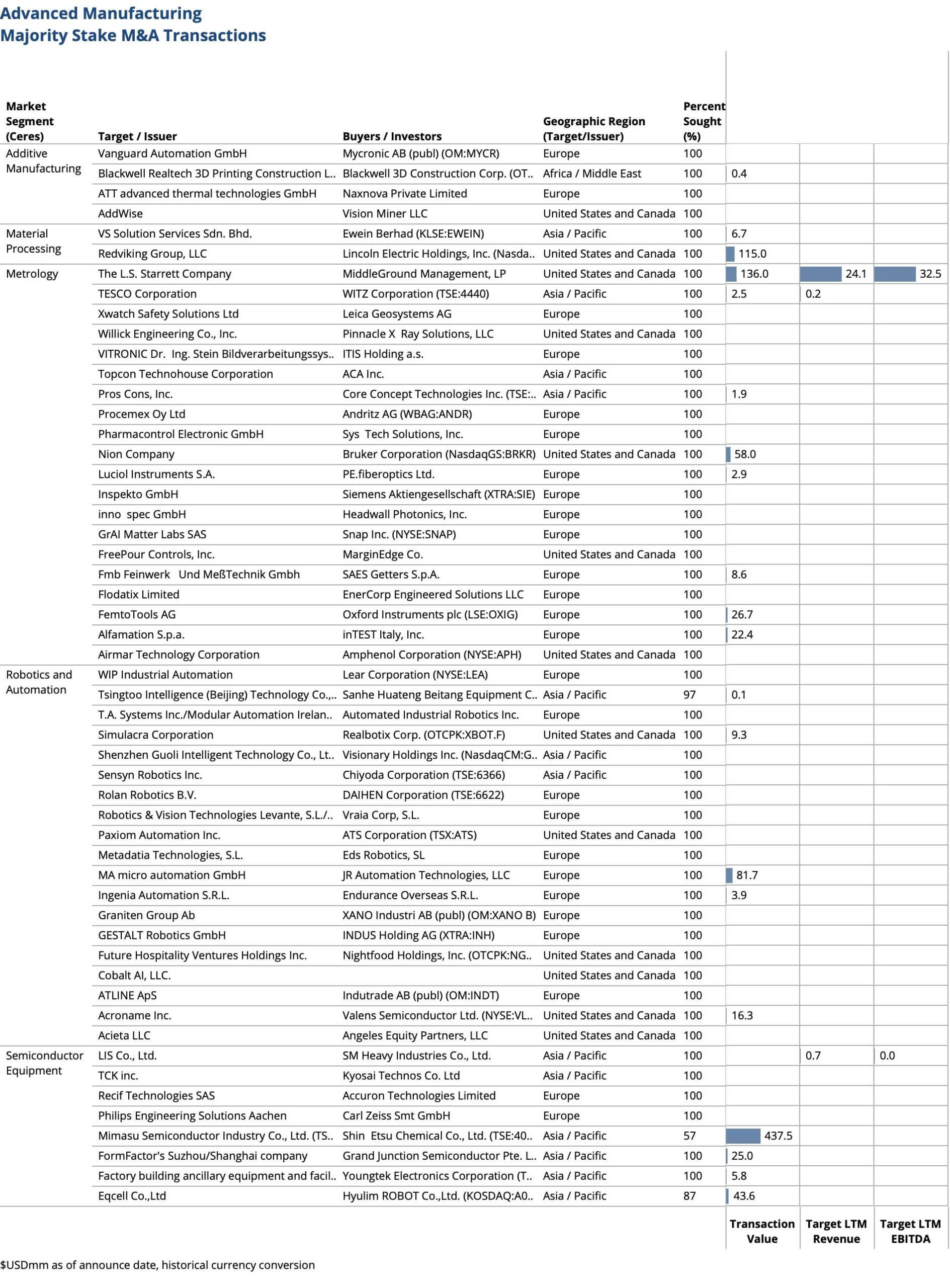

Advanced Manufacturing

Biophotonics

Defense, Security and Transportation

Information Technology

The Most Active Buyers

In line with history, the most active buyer is Bruker Corporation who acquires four Biophotonics companies – Nanophoton Corporation, provider of laser microscopes (3.50x $5M revenue); Spectral Instruments Imaging, LLC, provider of preclinical optical systems for bioluminescent, fluorescent and x-ray imaging (3.75x $10M revenue); Tornado Medical Systems, Inc., provider of optical spectrometers for raman spectroscopy and spectral-domain optical coherence tomography; and ELITech Group SAS, manufacturer of in vitro diagnostic equipment and reagents for $943M. Bruker also acquires Nion Company, manufacturer of scanning transmission electron microscopes (STEM)(7.25x $8M revenue).

Pure-play Photonics market leaders are not acquisitive in 2023 and 2024. With the exception of Ansys transaction, total and average value, as well as number of transactions are down substantially from 2021 highs. There continues to be a high concentration of strategic acquisitions of capabilities, product lines and technical talent. The first quarter 2024 uniquely sees a high concentration of financial buyers and strategic buyers owned by private equity firms. Private equity owned Luxium Solutions, LLC acquires PLX Inc., retroreflector manufacturer and Inrad Optics, Inc., optical components supplier.

2024 Photonics M & A

Despite a lot of economic and geopolitical uncertainty in the first half of 2024, M&A activity for targets employing photonics technology appears to be on a healthy upward trajectory – outpacing the global M&A market as a whole.

High interest rates, lower valuations and geopolitical instability are show-stoppers for many buyers and sellers, while fueling the strategic need for M&A to grow stronger, creating pent-up demand. The flood gates seem poised to open wide for photonics targets given their essential role is transforming and disrupting markets during these times of otherwise slow economic growth and uncertainty.

CERES sources transaction data from public sources. CERES analysis and data are subject to errors and omissions. Accuracy of information is responsibility of user.