Quantifying International Investment Risks

Understanding today’s country-specific cost of equity capital alongside industry dynamics help business valuation professionals advise clients in making better international investing, financing, and buy/sell decisions. A business identical in every way except the country in that it operates is valued differently by a buyer or investor depending on where that business operates. A buyer expects a higher return in exchange for the higher risk when acquiring a company that operates in a country that has higher financial, economic and/or political risk.

To value a cross-border transaction, country risk is mapped to a risk premium or discount that is added to the cost of capital relative to the cost of capital in the investor’s country and then applied to forecasted cash flows in an Income Approach to valuation.

Country Risk

They are three types of country-specific risk to consider when quantifying international cost of equity capital – financial, economic, and political.

Financial Risk

- Currency volatility and inability to hedge or convert currency

- Inability to repatriate profits

- Losses from foreign exchange controls

- Foreign trade collection history and delayed payment of suppliers’ credits

Currency Risk

Currency risk is the financial risk that exchange rates are volatile – changing suddenly and frequently. As a result, a US acquirer may expect a higher return when acquiring a company operating in a European country with higher currency volatility than when acquiring an identical company operating in the US. Higher currency volatility maps to higher financial risk and lower valuation.

Currency Conversion

Expected changes in exchange rates can often be hedged. However, even when currency hedging is used, exchange rate risk often remains.

When a company acquires across its borders, the returns the foreign acquirer experiences in local currency terms are identical to the returns a domestic acquirer would experience, however, the foreign acquirer faces the incremental risk in the form of currency risk when returns are brought back home and converted to its native currency.

Annualized Historical Returns for LTM June 30, 2015; MorningStar Price Indices for Large + Mid Cap Equities

As an example and referencing table above, because the EUR depreciated against the USD and other countries’ currencies during LTM (last twelve months) June 30, 2015, German-based acquirers investing abroad in countries where photonics industry players reside, experienced a higher return when they repatriated their returns and converted to Euros. On the contrary, US acquirers investing abroad experienced a lower return when repatriating returns and converting to USD. If currency risk cannot be hedged, the difference between returns in local terms (EUR, JPY, KRW…) and USD is the incremental increase in the cost of capital or currency risk premium. It is added to the discount rate that is applied to the target acquired company’s forecasted cash flows converted at forward-looking exchange rates.

Some research finds that exchange risks have a significant impact on total risk premium – especially in emerging markets, where exchange risks represent more than 50% of the total risk premium. Research also exists to support that despite not being constant, currency risk premiums are small and fluctuate around zero. So, rather than capturing the risk in the discount rate, it is more predictive to translate future cash flows into the native currency.

Economic Risk

- Volatility of the economy

- Current and expected inflation

- Debt service as a percentage of exports of goods and services

- Current account balance of the country where subject company operates as a percentage of goods and services

- Parallel foreign exchange rate market indicators

- Labor issues

Unsustainable Government Debt Loads

An economic risk that is in the spotlight is sovereign debt crisis. For example, the economic crisis in Greece has pushed governments globally to re-think their own fiscal policies as it becomes more obvious that current debt loads are likely not sustainable in many countries.

Lenders may demand higher expected returns to compensate for incremental default risk when investing in a country’s sovereign debt if it is considered unsustainable.

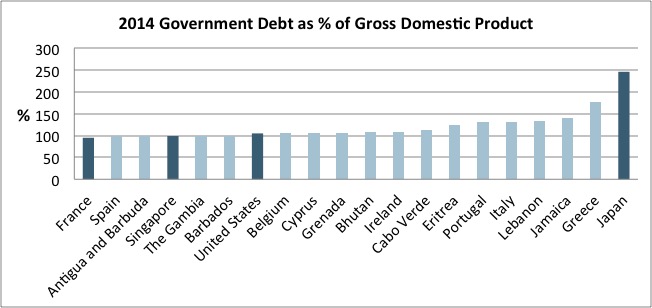

World Economic Outlook Database from the International Monetary Fund

The graph above depicts 2014 Government Debt as a percentage of Gross Domestic Product (GDP) for the 20 countries with the highest debt load to GDP ratios. Countries with the highest concentration of companies in photonics industry or industries enabled by photonics technologies, such as advanced manufacturing equipment, information technology, life sciences, and lighting, are highlighted among predominantly emerging or frontier country markets.

As an example, an investor may expect a higher return when acquiring a company operating in Japan, a country with relatively very high debt balance as a percentage of its exports of goods and services. An unsustainable amount of government debt maps to higher economic risk and lower valuation for companies operating in those countries.

Political Risk

- Renunciation of contracts by government

- Expropriation of private investments in total or part through change in taxation

- Economic planning failures

- Poorly developed legal system

- Political leadership and frequency of change

- Government corruption and poor quality bureaucracy

- Organized religion, military, and terrorism in politics

- Racial tensions and civil war

International Cost of Equity Models

They are several commonly used International Cost of Equity Capital models employed when valuing a business.

Capital Asset Pricing Model

Relevant broadly to both domestic and international investments in technology businesses, the Capital Asset Pricing Model (CAPM) often incorrectly assumes cash flows are predicted to be in a stable state growing in perpetuity at a constant and sustainable growth rate. Also, relevant to most domestic and international closely held private businesses, CAPM incorrectly assumes investments are held in a well-diversified portfolio. Thus, the overly simplified CAPM models are rarely applicable in valuing privately held technology businesses, home or abroad, where cash flows are rarely predicted to be in a stable state and the business is often the majority of a private owner’s undiversified portfolio.

Country Yield Spread Model

In this model, the Country Risk Premium (CRP) isolates the incremental risk associated with investing in a foreign market as a function of the spread between the foreign country’s sovereign yields and the home country’s sovereign yields denominated in the home country currency.

Where:

K e, foreign country = Cost of Equity in foreign country

R f, home country = Risk free rate on government bonds in home country

β home country = Beta in similar industry as foreign country’s subject company

ERP home country = Equity Risk Premium of home country

CRP = Country Risk Premium, difference between yield to maturity on government bonds in each country

Relative Volatility Model

In this model, the home country’s market equity risk premium is adjusted by the Relative Volatility (RV) factor. The RV factor isolates the incremental risk premium as a function of the relative volatility of the foreign country’s equity market and the home country’s equity market.

Where:

RV = Relative Volatility Factor, ratio of annualized monthly standard deviation of foreign country equity returns to that of home country equity returns

Country Credit Rating Model

This model is based on the assumption that countries with lower credit worthiness, which is translated into lower credit ratings, are associated with higher costs of equity capital.

Cross Border Valuation Perspectives

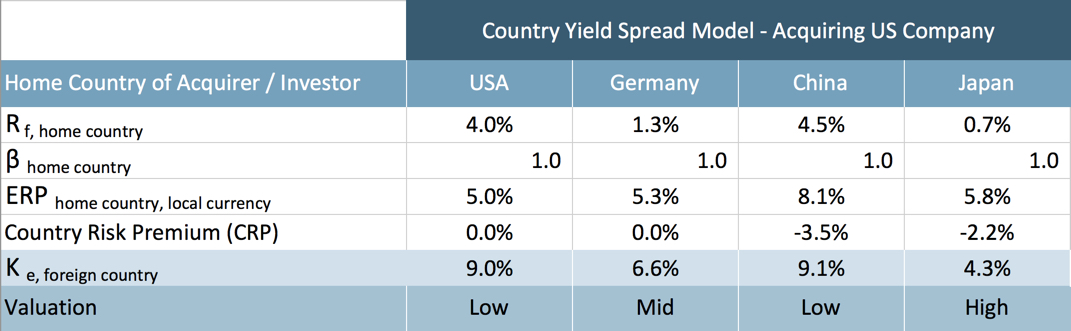

Applying the Country Yield Spread model to compare the valuation perspectives for acquirers located in US, Germany, China and Japan, the cost of equity capital is lowest in Japan and highest in US and China. Thus, all else equal, the US and China based investors will value the US target company less than will the German and Japan based investors.

Strategic Cross Border Transactions

The comparisons above assume all things are equal except the home countries of the acquirer and the home country of the target company. All things are never equal.

A cross border strategic, as opposed to purely financial, transaction is most often pursued to gain access to a distribution channel, a low cost supply chain, a technology cluster, government regulatory freedoms, or a well known premium brand in untapped geographies. Incremental strategic value is paramount. Financial implications of country risks are considered after strategic value is identified; however, they are critical to structuring the transaction and valuing the acquisition or investment.

Sources: International Valuation Handbook – Guide to Cost of Capital (Duff and Phelps); Credit Suisse Global Investment Returns Sourcebook; Market Risk Premium and Risk Free Rate used in 88 countries: a survey with 8,228 answers (Pablo Fernandez).