Intellectual Property, Research, New Ventures

Monte Carlo simulation is a well established method for simulation in engineering models – including raytracing and tolerancing of optical systems. Monte Carlo simulation, Real Option, and other advanced mathematical methods are being applied more and more to financial modeling and valuation of high risk, intangible assets such as intellectual property, R&D, and venture capital financed businesses.

Traditional Discounted Cash Flow (DCF) methods that employ a single discount rate regardless of risk mitigation as time passes and static forecasts assuming absolute certainty and no option of abandonment often yield valuation conclusions that not even the most risk tolerant investor, product manager or CEO would tackle. Yet, these high risk opportunities can offer enormous rewards. See how these advanced methods give insight at critical decision points and better account for high risk, high reward intangibles in early stage financings, impaired asset judgments, and licensing transactions.

Case: Nanotechnology for Solar Energy Concentration

Consider a fictitious IP portfolio of nanotechnology applied to solar energy concentration. The basis of its value is the potential cash flows from licensing-out. Assume the technology will be exclusively licensed to a chemical company who will commercialize and manufacture a product that will make solar energy concentrators more efficient.

The forecasted royalty rate is 5%, an estimate that considers the 25:75 rule-of-thumb and guideline industry comparable royalty rates.

.png){kind=link}

Addressable market size and average selling price (ASP) are obtained from third party analyst reports, primary research, and weighting competitive product differentiation. Its commercialization potential is reflected by a forecasted market adoption S-curve. The forecasted end product ASP is $1 per square foot of addressable solar concentration area.

{kind=link}

Proformas include R&D investments, cost and reimbursement of technology transfer, business development and marketing costs, and corporate and patent legal fees. A pure royalty deal structure is assumed with no minimum royalty, kicker, or termination fees. Cash flows also reflect a raw material supply agreement. A quick calculation concludes that executing a raw material supply agreement with the licensor adds significant value with nominal additional risk and upfront investment. The licensor purchases raw material from licensee ar a price of 10% ASP. Cost of raw material is 2% ASP.

Traditional Discounted Cash Flow Analysis

A traditional discounted cash flow analysis applies a single discount rate to the proforma licensing-out cash flows. Based on heuristic discount rates used in technology and license negotiations, the forecasted cash flows that result from licensing-out the technology are discounted at 45%. The risk is assumed “very high”, because it requires development of a new product using a not well understood technology. Risk is not considered “extremely high”, because solar concentrators exist today, although they are not currently marketed to this segment with these features and benefits.

{kind=link}

This traditional DCF analysis yields a sinlge point negative valuation of -$1.5 million.

Monte Carlo Analysis

Employing a Monte Carlo simulation method, probability distributions are applied to variables in the forecast model to reflect uncertainty in assumptions. In this case, probability distributions are applied to ASP, addressable market, market adoption, royalty rate, and raw material COGS.

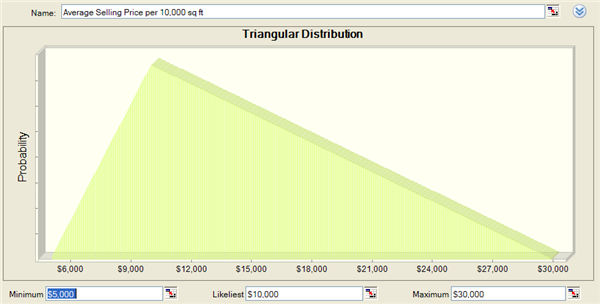

The average selling price is assigned a triangle distribution with most likely, minimum, and maximum values of $0.50, $0.30 and $3.00 per square foot.

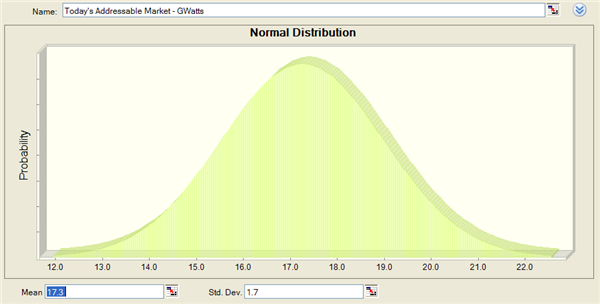

Today’s addressable market size is assigned a Gaussian distribution with a mean of 17.3GWatts and standard deviation of 1.7GWatts. The average annual forecasted growth rate three years and beyond after launch was assigned a triangular distribution with most likely, minimum, and maximum values of 5%, 0% and 10% to reflect difference in third party analyst long term forecasts.

Forecasted peak market share and market share at 2 and 5 years post product launch are two variables that significantly drive the market adoption curve. Peak market share is assigned a triangular distribution with most likely, minimum, and maximum values of 20%, 5% and 40%. Market share post product launch at critical decision points are also assigned triangular distributions.

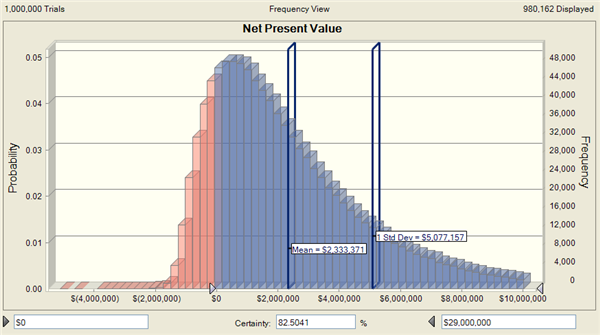

Applying the same 45% discount rate, reflecting “very high” risk, the Monte Carlo simulation yields a valuation range with a mean of $2.3 million and within one standard deviation of $0.5 and $5 million. The simulation yields a greater than 80% probability that the project would break-even or better.

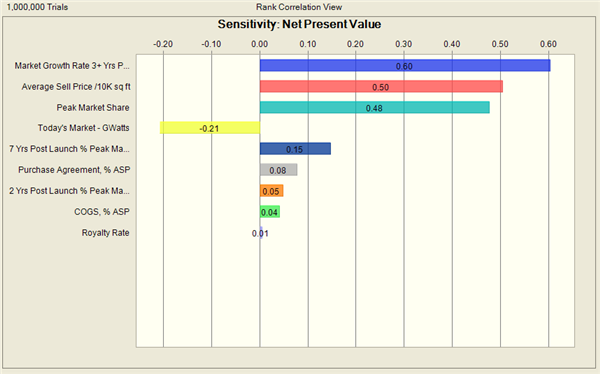

A sensitivity analysis on the simulation shows that uncertainty around the addressable market dwarfs other contributions to the variance, such as royalty rate, raw material cost of goods sold, and raw material selling price. In addition to a valuation range, the simulation and subsequent sensitivity analysis yield insight as to what uncertainties drive the valuation and where to focus when mitigating technology or market risk in positioning the technology in license negotiations.

Assessing Risk with Monte Carlo Simulation

Like Real Option Valuation (ROV) methods, Monte Carlo simulation applied to DCF can accommodate options of abandoning or investing more over time. It is also applied to models with variable discount rates that reflect variable risk over time. Applications include pharmaceuticals and other products with high market risk requiring significant R&D investments.

Monte Carlo simulation applied to decision trees facilitates the understanding of overlapping probability profiles of multiple options to assess risk in decision making. An application is the decision to litigate or do nothing when a competitor is successful selling a product believed to infringe on valid patents. The model includes probabilities of validity and infringement as well as royalties and costs of full litigation and settling.

Applications

Advanced mathematical methods are used today to value high risk intangible assets and to assess risk in decision making. Practical applications include impaired asset judgements when acquiring goodwill and a thin balance sheet, licensing transactions, acquisitions of technology companies, patent litigation, valuation of customer relationships and R&D, early stage financings, and technology product planning. Not unlike accepted engineering models, the calculated values are only as predictive as the inputs; regardless, assigning probabilities to reflect input uncertainties yields critical insights.