Small and Middle Market Consolidation

M&A activity in the photonics industry continues with the volume of transactions in the first four months of 2013 in pace with 2012.

The trend of small and middle market consolidation in the highly fragmented photonics industry, as well as in the vertical market segments it enables, persists. Given uncertainty around the future role of government regulation and fiscal policy, and better than expected first quarter US corporate earnings accompanied by weak revenue growth, it is likely that organic growth will remain muted and strategic buyers will continue to absorb targets – sustaining the pattern of consolidation through 2013.

Activity

M&A transactions for target companies are researched with closing or announce dates from January 1 through May 3, 2013. Values are in $US at historical rates of exchange. Follow this link to transaction detail. <2013 Jan to May Photonics M&A Transactions>

The Medical Imaging, Medical Diagnostics, Display, Communications, Metrology for Advanced Manufacturing, and LED Luminaires segments saw the most activity in volume of transactions.

The Energy segment that includes the Solar value chain – wafers, cells, panels, systems – also experiences a high volume of transactions. Compared to 2012, the Solar sector realizes higher valuations. This may be indicative that consolidation is strengthening the industry.

M&A Transaction Volume

Photonics & Vertical Markets Served

January – May 2013

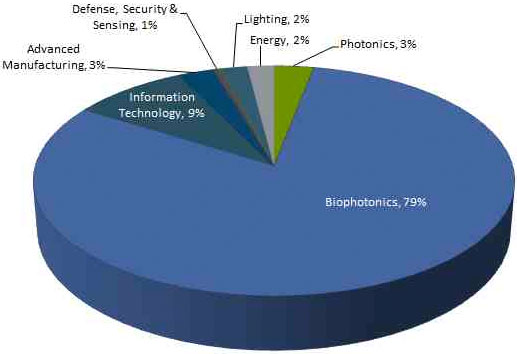

The total reported transaction value by sector is heavily weighted by a single large transaction. In Biophotonics, specifically Life Sciences – Life Technologies Corporation, supplier of biotechnology tools and consumables, is acquired by Thermo Fisher Scientific for $16billion.

Lighting, Defense, Security & Sensing, Advanced Manufacturing and Photonics segments combined see less than 10% of the total value of transactions.

Transaction Value

Photonics & Vertical Markets Served

January – May 2013

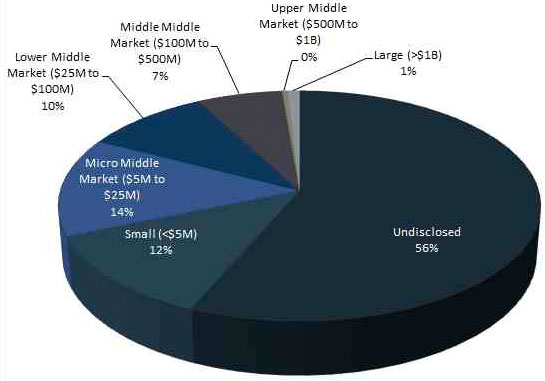

Transaction by Size

Small and Middle Market Transactions

43% of researched transactions disclose the transaction value. Of those disclosed, greater than 80% are small market (<$5M), micro middle market ($5 to $25M), and small/middle market ($25 to $100M).

Since 2010, the lower and middle of the M&A middle markets remain robust. These researched transactions are consistent with that market as a whole. However, uniquely, in the Photonics sector and the vertical market segments enabled by photonics, strategic buyers are acquiring orders of magnitude smaller businesses providing products that are highly differentiated with strong intellectual property positions.

M&A Transaction Size

Photonics & Vertical Markets Served

January – May 2013

Strategic vs. Financial on Buy and Sell Side

Like 2012, the vast majority of transactions by volume and value are strategic. However, financial investment firms are more active in 2013 than 2012 – up to 9% from 3% of transactions involving financial investment buyers and down to 8% from 12% involving financial investment sellers. This is evidence that strategic premiums in valuation remain healthy in 2013.

Valuations

In 2013, the total and average Enterprise Value of the 100 transactions reporting financial data are $27.5 billion and $299 million respectively. While the total volume of transactions is in line with 2012, the average Enterprise Value is more than doubled due to the Thermo Fisher acquisition. Removing this transaction from the analysis, the average Enterprise Value of $129 million is in line with 2012 and is evidence of a robust market for smaller transactions.

Compared to the 2012 simple average of reported Implied Enterprise Value to EBIT, EBITDA and Revenue multiples of 19.5, 21.1 and 1.9 respectively, the simple average of 2013 Revenue and EBITDA multiples are significantly higher. Implied Enterprise Value includes implied equity value, earn-out and contingent payments, rights, warrants, options, and net assumed liabilities adjusted for size.

Average Enterprise Values in the first four months of 2013 are up over 2012. Biophotonicssector realizes the highest average multiple of Enterprise Value to Revenue, 9.2 (7.1 in 2012), while Energy/Solar realizes the lowest, 1.3 (0.7 in 2012).

Few transactions report financials and the average Biophotonics sector multiples are skewed high by a single transaction in the Imaging segment. Progenics Pharmaceuticals acquired Molecular Insight Pharmaceuticals, a clinical-stage biopharm company commercializing imaging oncology radiopharmaceuticals for 36x Revenue of $4million. However, when removing this transaction from the average, the average Enterprise Value to Revenue remains relatively high at 2.6.

The Ligthing sector also realizes a relatively high average Enterprise Value to Revenue of more than 3.6. This is driven high by the LED Luminaires segment. For example, Evolucia acquires Affineon Lighting, supplier of architectural LED fixtures and control systems, for 6.0x revenue of $4million.

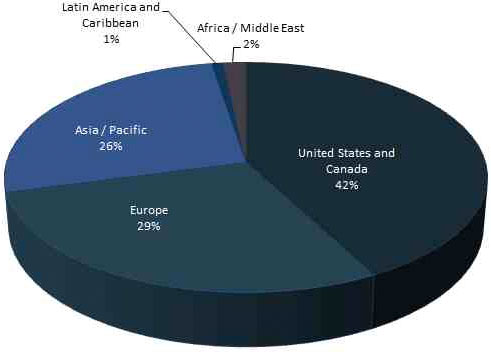

Geography

The United States and Canada, as a geographical region, experience the most buy and sell side activity. More than 25% of transactions represent buyers acquiring targets outside their geographical region.

M&A Transactions by Geography – Target

Photonics & Vertical Markets Served

January – May 2013

M&A Transactions by Geography – Buyer

Photonics & Vertical Markets Served

January – May 2013

Most Active Buyers

Highlighted below are the most active buyers by volume and size of transactions. In 2012, more than 20 micro and middle market strategic buyers acquired two or more entities – indicative of highly strategic and not opportunistic buys. In contrast, for the first four months of 2013, upper middle and upper market buyers account for the lion’s share of transaction value.

The Transactions

Follow this link to transaction detail. <2013 Jan to May Photonics M&A Transaction Detail>